Economic Watch: Industrial Production, Consumer Sentiment Up; New Homes Mixed

Industrial production in the U.S. rebounded from a drop at the start of the year, as consumer sentiment is the best in more than a decade – but there's a decline reported in parts of the new-home-building market.

Industrial production in the U.S. rebounded from a drop at the start of the year, as consumer sentiment is the best in more than a decade – but there's a decline reported in parts of the new-home-building market.

The Federal Reserve reported the total amount of output from the nation’s factories, mines and utilities rose 1.1% in February following a decline of 0.3% in January. The latest performance was better than analysts’ expectations, with the gauge posting a year-over-year gain of 4.4%.

Manufacturing production rose 1.2% in February, its largest gain since October, while the January performance was revised downward for a 0.2% decline.

Gains were recorded by every major manufacturing industry except for electrical equipment, appliances, and components, and for petroleum and coal products. The production of durables climbed 1.8%, and the measure for nondurables moved up 0.7%.

Mining output jumped 4.3%, mostly reflecting strong gains in oil and gas extraction, while the output from utilities fell 4.7%, as warmer-than-normal temperatures last month reduced the demand for heating.

At 108.2% of its 2012 average, total industrial production in February was 4.4% higher than it was a year earlier.

Capacity utilization for the industrial sector climbed 0.7 of a percentage point in February to 78.1%, its highest reading since January 2015 but still 1.7 percentage points below 1972–2017 average.

Analysts at Econoday noted manufacturing looked "very positive with strength centered in business equipment, where rising production points to rising business investment, and also construction supplies which are in demand as builders restock the housing sector. Production of vehicles also picked up, as did the selected high-tech sector which, like mining, has been an important positive for the industrial sector.”

Housing Starts Drop Due to Multi-Family Sector Plunge

In sharp contrast, housing starts in the U.S. plunged more than expected during February, posting a 7% drop from the month before, according to the Commerce Department.

This put the adjusted annual rate at 1.24 million units, down from an upwardly revised January level of 1.33 million, which was the highest level in more than a year.

The market was pushed lower for the second straight month by a drop in the volatile multi-family home sector, which fell 26.1%. Single-family home starts, the biggest share of the market, increased 2.9% from the revised January level.

The number of home-building permits issued during February, an indicator of future construction, fell 0.6% for single family homes while those for multi-family homes declined nearly 15%.

The overall pullback in home starts was not surprising following January’s strong performance, according to Katherine Judge, economist at TD Economics. She noted single-family starts posted another gain in February and permits remain elevated relative to 2017, indicating that activity should continue at a brisk pace this year.

“Barriers to activity remain, however, including a continued labor shortage in the construction industry and a lack of buildable lots,” she said. “Additionally, tax reforms that cap the state and local tax deduction and lower the mortgage interest deduction will work to shift demand to lower-priced segments of the market. That won't alter the number of housing starts; however, the value per unit under construction is expected to decrease as a result.”

Consumer Sentiment Best Since 2004

Meantime, a preliminary report also released Friday showed consumer sentiment rose in early March to its highest level since 2004 due to a new all-time record favorable assessment of current economic conditions, according the University of Michigan Survey of Consumers.

All of the gain in the Sentiment Index was among households with incomes in the bottom third. In contrast, the economic assessments of those with incomes in the top third posted a significant monthly decline. The decline among upper income consumers was focused on the outlook for the economy and their personal finances.

Consumers continued to adjust their expectations in reaction to new economic policies, said Richard Curtin, the survey’s chief economist.

"In early March, favorable mentions of the tax reform legislation were offset by unfavorable references to the tariffs on steel and aluminum. Each was spontaneously cited by one-in-five consumers,” he said. “Importantly, near-term inflation expectations jumped to their highest level in several years, and interest rates were expected to increase by the largest proportion since 2004."

Curtin said these trends have prompted consumers to more favorably cite buying as well as borrowing in advance of those expected increases.

“While income gains are still anticipated, the March survey found that the size of the expected income increase returned to the lows recorded in the past year,” Curtin said. “Among the top-third income households, income expectations fell more and inflation expectations rose more, as these households account for more than half of all consumption expenditures. The data suggest that the relative lull in consumption in the first quarter may persist for another quarter.”

More Fleet Management

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

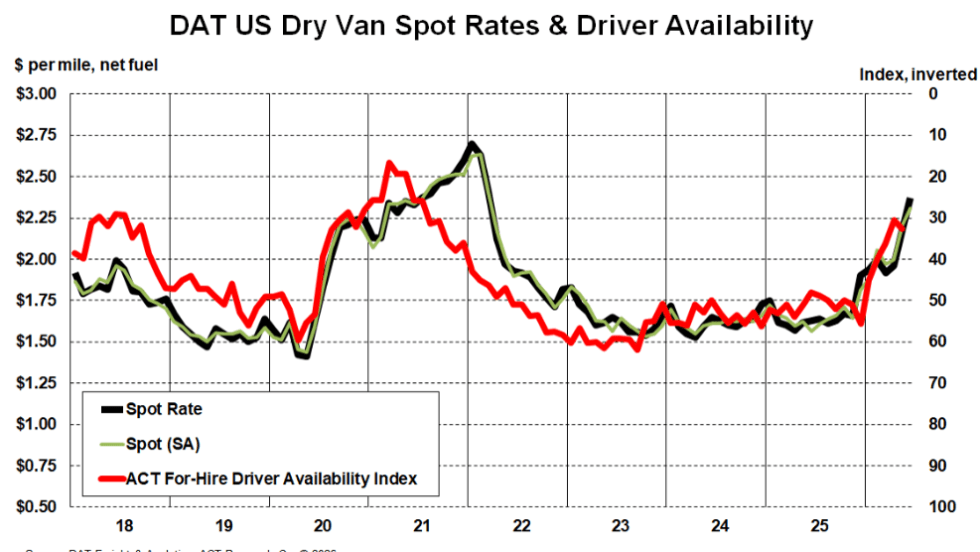

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

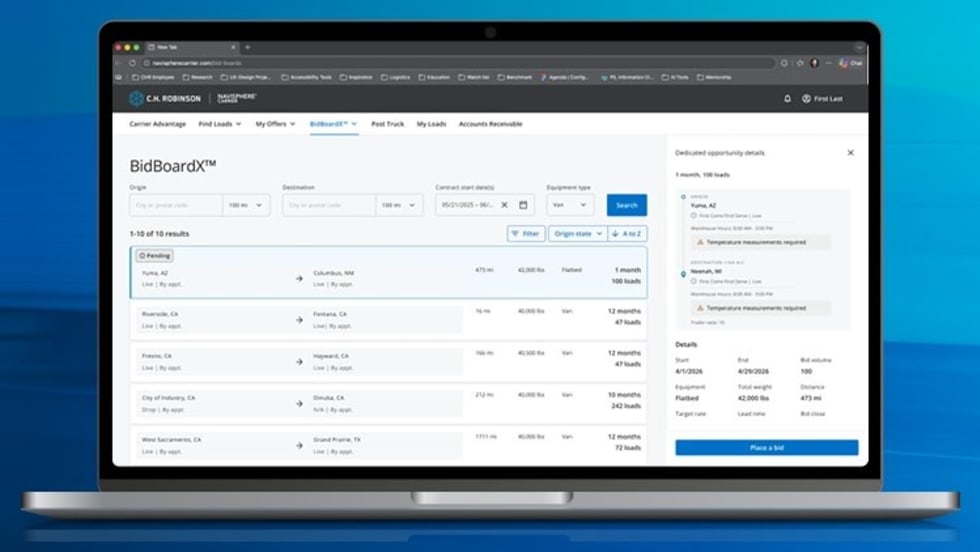

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →