Freight Index Disappoints After Offering ‘False Hope’

After offering a glimmer of “less bad” hope in August, one measure of freight shipments data in September disappointed.

Evan Lockridge・Former Business Contributing Editor

October 19, 2016

4 min to read

After offering a glimmer of “less bad” hope in August, one measure of freight shipments data in September disappointed -- although there are a few areas of growth.

Turns out that September report was "false hope," says the author of the monthly Cass Freight Index Report, Donald Broughton, who's managing director, chief market strategist and senior transportation analyst at the investment firm Avondale Partners.

Ad Loading...

“September data is once again signaling that overall shipment volumes and pricing continued to be weak in most modes, with increased levels of volatility as all levels of the supply chain – manufacturing, wholesale and retail – continue to try and work down inventory levels," said Broughton.

“That said, there have been a few areas of growth, mostly related to e-commerce, with lower levels of expansion being experienced in transit modes serving the auto and housing/construction industries."

In the Cass Freight Expenditures Index, expenditures (the total amount spent on freight) were up month-over-month in August, and the year-over-year rate of contraction appeared to be ‘less bad’ than the rates in May, June, July, and August.

Ad Loading...

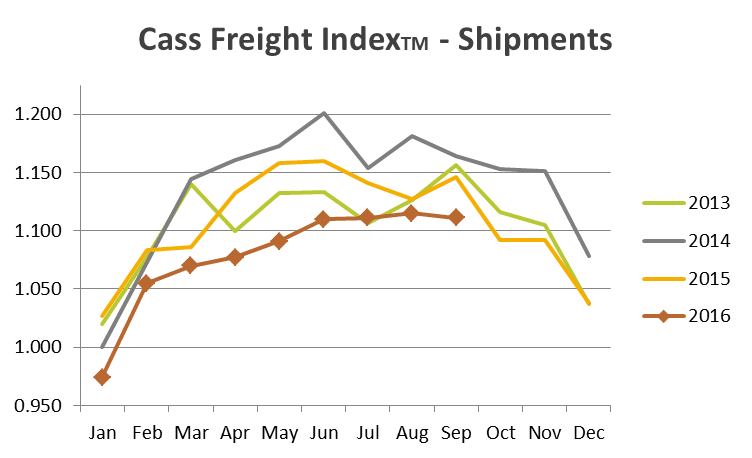

In September, however, index measurements for freight shipments and expenditures fell 3.1% and 3.8%, respectively, compared to a year ago. It was the 19th straight month of shipment declines. Shipments dropped 0.4% last month from August. Expenditures rose 5.2% month over month, but Broughton said this was the result of the steady increase in the price of fuel over the last six months and not an increase in pricing power.

Broughton said continued weakness in freight movements is being driven by the excess of capacity in most modes, whether you're talking about trucking, rail, air freight, barge, ocean container or bulk.

“Although at first blush it appears that in most modes the gap between spot pricing and contract pricing appears to be closing slightly, this is more a function of slight declines in contract pricing than it is a function of improvements in spot pricing,” he said. “We see little reason to predict a change in course or material strength in either the contract or spot rates for most modes. Exceptions to this do remain in the parcel marketplace and forms of expedited transit supporting e-commerce.”

All this, he said, is happening against a backdrop of the U.S. economy in a state of transition.

“After the explosion in fracking activity drove the first industrial-led recovery from 2009-2014 in the U.S. since 1961, we have been patiently waiting for the consumer to take the baton of leadership in economic growth,” Broughton said. The lower fuel prices didn't prompt consumers didn’t go out and spend freely, though.

Ad Loading...

“U.S. consumers have been choosing to pay down debt and increase their savings rate. Simply put, the consumer has not yet picked up where the industrial economy left off,” Broughton said.

Adding to these problems for the economy and trucking is that inventories have been bloated, subtracting from total U.S. gross domestic product growth to the tune of around 3% the past five straight quarters. However, Broughton is somewhat optimistic inventories will fall.

He did sound an alarm about increasing talk about the Federal Reserve raising interest rates, possibly before the end of the year. His concern is that will make the already strong U.S. dollar even stronger, and that could hurt the overall economy and freight.

“Historically, a strong dollar has produced a serious headwind for freight volumes, first in all things exported, and then in a reduction of things manufactured or assembled domestically,” he said. “Nothing in the freight flow data suggests that another rate hike is warranted, or even that the first hike in December 2015 was necessary.”

On the consumer side of the equation, Broughton sees some signs of hope, especially for those retailers with a strong e-tailing or omni-channel offering.

Ad Loading...

“With the price of oil and natural gas remaining low, we see little reason to predict a resurgence in fracking or the many types of industrial activity that fracking drives. Obviously, this would also mean that the consumer would continue to enjoy improved disposable income,” he said. “As we have pointed out, the U.S. consumer has been saving and paying down debt with this disposable income for over six quarters. By this holiday season, we expect them to begin to spend at least part of their income. If not, the risk of an overall recession grows.”

When the unexpected happens, how you react to, and deal with operational blind spots is critical. Here’s how to keep you recovery on track, when nothing is normal.

As fleets adopt artificial intelligence for routing, maintenance, and load matching, new security risks are emerging. Learn where the vulnerabilities are and how to put the right controls in place.

CargoNet reports fewer supply chain crime events to start 2026. But losses hold steady as organized crime shifts tactics toward impersonation schemes and high-value goods.

Heavy Duty Trucking is searching for forward-looking leaders at trucking fleets as nominations for HDT’s Truck Fleet Innovators 2026. Deadline is May 15.

Cargo theft rings plant operatives as drivers inside legitimate, fully vetted carriers, then execute coordinated thefts that look like a traditional straight theft from the outside.

The American Transportation Research Institute will examine driver coaching, regulatory impacts — including the "Beyond Compliance" concept —and weather disruptions that shape trucking operations.

Fleet Advantage's Brian Antonellis says it's time for fleets to get back to the fundamentals of good maintenance practices. And that includes replacing older, inefficient equipment.