You Also May Like: Are You Setting Your Rate the Right Way?

Has the Freight Cycle Peaked?

High fuel prices and inflation are among the factors prompting analysts to say the freight pendulum is starting to swing back the other way.

May 17, 2022

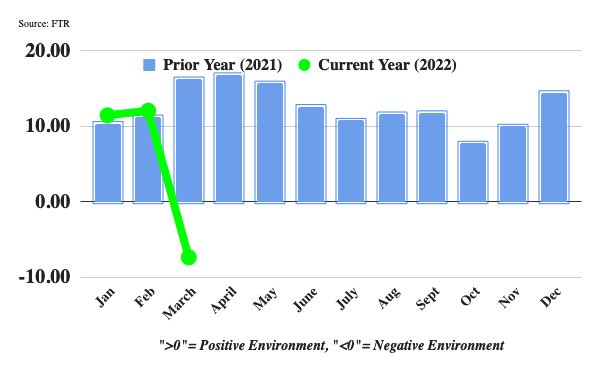

FTR's Trucking Condition Index took a major plunge in April.

Source: FTR

3 min to read

It appears the freight cycle is heading back down, with fuel prices, inflation, and global uncertainties putting a drag on both trucking and the economy.

FTR’s Trucking Conditions Index for March was negative for the first time since May 2020, caused by record diesel prices and, to a lesser extent, weaker freight rates.

The Index plunged to a reading of -7.38 from February’s positive 12.06 reading. The TCI tracks the changes representing five major conditions in the U.S. truck market: freight volumes, freight rates, fleet capacity, fuel prices, and financing costs.

Although the outlook for trucking conditions generally is for modestly positive conditions, FTR said, uncertainty is rising in several key areas, including fuel costs, capacity utilization, and rates.

“Given the unprecedented surge in diesel prices during early March, a negative reading for the Trucking Conditions Index was hardly surprising,” said Avery Vise, FTR’s vice president of trucking. “Fuel costs apparently will represent a big negative factor for May as well.”

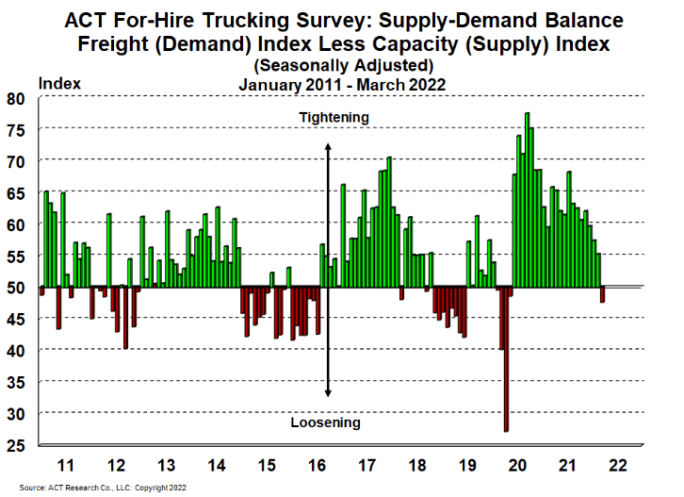

The pendulum of the freight cycle is swinging back, said ACT Research in its latest freight forecast.

ACT's supply-deman balance survey loosened in March for the first time since 2020.

Source: ACT Research

“As recently as the start of the year, pricing power in the truckload market was firmly with fleets,” said Tim Denoyer, ACT senior analyst. “But once a pendulum gets going, it’s very hard to stop.”

ACT reported that the supply-demand balance in its for-hire survey turned loose this month for the first time since June 2020, “as the rebalancing, drawn-out by the pandemic, hit critical mass," Denoyer said.

The Driver Shortage and Spot Rates

“The driver shortage is over,” said ACT’s Denoyer. “The record drop in spot rates ex-fuel in the past few months has been magnified by Russia and Omicron, but still clearly says the market has shifted to a driver surplus. We’re not adding nearly as much equipment capacity as we typically would, which suggests a possibly shorter-than-normal downcycle.”

FTR’s Vise noted that a stronger supply of drivers is enabling a shift of activity back to the contract environment from spot, but overall freight volume so far has remained strong.

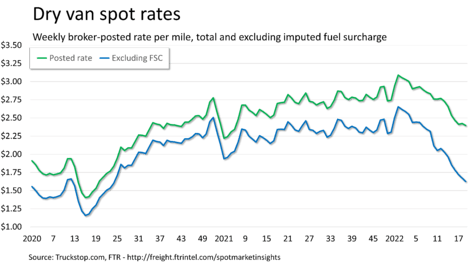

When you take out the fuel surcharge, dry van spot rates have been sliding most of the year.

Source: Truckstop.com

Spot rates for dry van and refrigerated freight have been sliding in the Truckstop.com system for most of 2022. As of its May 16 report, dry van spot rates are down about 69 cents from the record level posted at the end of 2021. Dry van rates were nearly 12% lower than the same 2021 week — but nearly 31% lower if the fuel surcharge is excluded. It’s a similar story with refrigerated spot rates, down nearly $1.33 since hitting a record at the end of 2021, 16% below the same 2021 week but about 33% lower excluding the fuel surcharge.

Contract rates, according to Uber Freight’s Transplace, remain elevated and have not yet followed the spot-market downward trend.

What About the Economy?

ACT’s Denoyer said while the freight sector is a leading indicator, “it’s mainly for the goods economy, rather than the larger service sector. Russia’s war has a tough-to-quantify but clearly adverse macro impact, and softer freight volumes are consistent with a slower economy.”

Vise pointed out that consumer spending is still robust even when adjusted for inflation, and industrial activity is growing.

In the near term, Vise said, “the larger uncertainties relate to potential external shocks — such as the pandemic-related lockdowns in China — and the fate of small carriers that are seeing weaker spot rates and soaring fuel costs. A flood of those drivers back to the security of working directly for larger carriers might accelerate a market normalization, although equipment availability could limit a downside on utilization and rates.”

Kenny Vieth, ACT president and senior analyst, said “the economy is walking a fine line in 2022,” with the effects of inflation, uncertainty about the war in Ukraine, and the impact of Chinese COVID lockdowns on global supply chains. Trucking industry profits tend to lag the freight cycle, so are likely to peak around the third quarter of 2022, he predicted.

“The road ahead looks treacherous, but it is not necessarily bad for carriers,” said FTR’s Vise.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →