More from FTR: Ukraine Invasion Increases Downside Risks to Trucking Conditions

Trucking’s Inflation Worries Go Beyond Fuel

For trucking companies, the biggest single threat from inflation arguably is not in their own costs, but in what higher costs will mean for consumer spending.

by Avery Vise, FTR

March 29, 2022

Some economists are skeptical that the Fed’s moves to address inflation will work, because the inflationary pressures are not normal.

Source: FTR

3 min to read

March’s unprecedented surge in diesel prices was one more indication that costs for truck fleets are rising sharply. Of course, the same is true for everyone. Consumer inflation is running at the highest levels in 40 years, prompting the Federal Reserve to raise the target federal funds rate for the first time since 2018 in a bid to cool things down a bit and return the economy to a long-run inflation rate of around 2%.

Inflation currently is running close to 8% annualized, and it’s still more than 6% if we exclude the volatile food and energy sectors. One reason economists exclude those sectors is that they tend to fall outside of usual pricing pressures. Food costs often vary because of weather-related issues such as droughts, floods, or freezes. Meanwhile, petroleum is a global economy that moves for a host of supply, demand, and political reasons or — as is currently the case — because the world’s third largest supplier of crude decided to start a war.

Some economists are skeptical that the Fed’s moves to address inflation will work, because the inflationary pressures are not normal. Much of it is driven by supply chain disruptions causing scarcity — a dynamic that we historically had seen just in food or a few other limited products at any given time. During the rebound from pandemic, however, these disruptions have become widespread.

How is inflation affecting trucking companies?

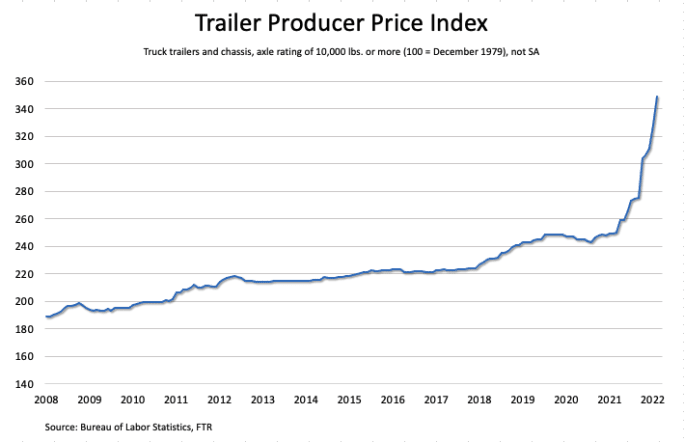

For motor carriers, inflation is showing up in places besides driver wages and fuel. Perhaps the most dramatic example is trailers. The Producer Price Index (essentially a measure of business-to-business inflation) for truck trailers and chassis has been surging for a year. February saw the second-largest monthly increase (6.3%) in the trailer PPI, after the third-largest increase (5.5%) in January. The largest one-month gain (10.5%) occurred in October. Surging trailer costs are not surprising given the price surges we have seen in key trailer materials, such as aluminum, steel, and lumber.

The Producer Price Index (essentially a measure of business-to-business inflation) for truck trailers and chassis has been surging for a year.

Source: FTR

For trucking companies, the biggest single threat from inflation arguably is not in their own costs, but in what higher costs will mean for consumer spending. If consumers buy fewer goods because each item they purchase costs more, that’s a loss of freight. That weakening of freight, in turn, would be compounded by the fact that retail inventory levels (except in the automotive industry) have risen sharply.

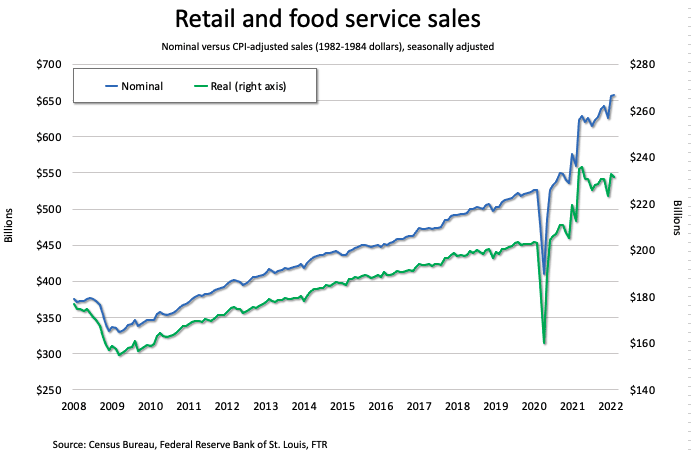

In February, retail and food service sales edged up to a record, but there are some nuances that should concern carriers. First, gasoline station sales were by far the strongest retail sector, and that was all due to rising prices. That obviously continued in March, although we do not have the data yet. If we exclude gas station sales, retail sales declined.

Pricing is a broader concern. Adjusted for the Consumer Price Index, retail and food service sales fell 0.5% in February, according to the St. Louis Federal Reserve. February sales in current, or nominal, dollars in February were 25.2% higher than February 2020. Real retail and food service sales were 14.1% higher than February 2020, according to St. Louis Fed figures. Both comparisons are well ahead of trend.

Higher costs clearly are a concern at any time, but robust rates have dampened those concerns some. The worry is that the negative effects of inflation on consumer spending could lead to less volume and, ultimately, weaker freight rates.

This article appears in the April 2022 issue of Heavy Duty Trucking.

Subscribe to Our Newsletter

More Fleet Management

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →

FTR Says Freight Rates Surged in May

FTR's Trucking Conditions Index surged to a record high in May, the analytics firm reports.

Read More →