What’s Going On with Fleet Employment Numbers?

For trucking companies struggling to find drivers, these numbers might sound like nonsense. And in fact, the truth is far more complicated.

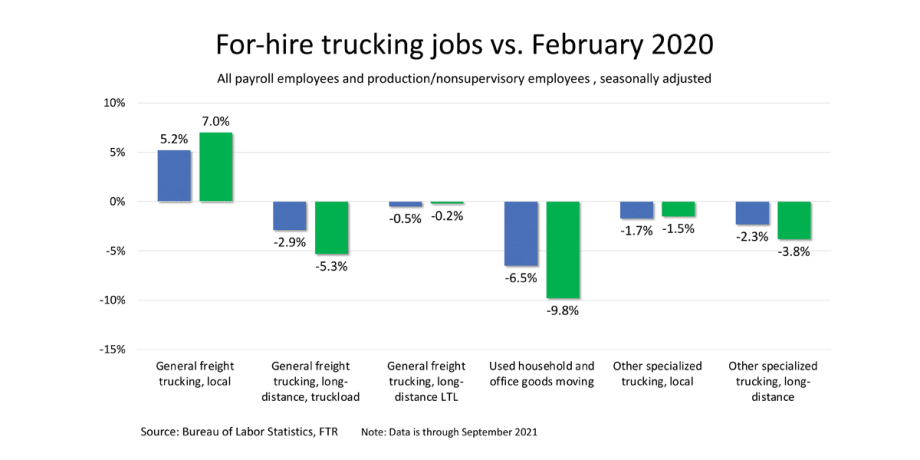

Note: Data is through September 2021

Source: Bureau of Labor Statistics, FTR

The for-hire trucking industry’s employment levels have recovered in fits and starts from the pandemic-related contraction in March and April 2020. Before the Bureau of Labor Statistics released its employment situation report in early November, it had appeared that payroll employment was still down about 22,000 jobs, or 1.4%, from February 2020, seasonally adjusted. Trucking certainly had recovered more jobs than many industries, but it seemed months away from returning to pre-pandemic levels.

The BLS report, however, showed solid growth for-hire trucking during October, adding in 7,900 payroll jobs. And the preliminary figures for August and September were revised sharply higher. So rather than being down nearly 22,000 jobs, trucking was down just 9,300 payroll jobs, or 0.6%, compared to a pre-pandemic February 2020. That might not be full recovery, but it is darn close.

For trucking companies struggling to find drivers, these numbers might sound like nonsense. And in fact, the truth is far more complicated.

First, the BLS numbers represent total employees, not drivers. Nevertheless, we generally treat payroll employment as a proxy, because it is the closest measure we have to real-time data and because drivers make up the lion’s share of workers.

Local vs. long-haul

Another limitation in the most up-to-date figures is that they do not tell us how different segments of the industry are faring. If we look back a month at September numbers, we can get more granular. We can look at “production/nonsupervisory employees,” which in trucking gets us closer to the truck driver population. We also can look at data for local and long-distance trucking in both general freight and specialized freight.

When we view the data through these prisms, it is much easier to reconcile the recruiting struggles of long-haul truckload carriers with what appears in the very broad picture like nearly full recovery.

Total trucking employment in September was 1.1% below February 2020, but those production/nonsupervisory employee jobs were still down 2.3%. This implies that drivers are a drag on trucking’s recovery, not a contributor to it.

Nor has the recovery been uniform across industry segments. All segments of trucking in the BLS data were down in September — except for local general freight trucking, which has seen a 5.2% increase in total payroll employees and a 7% increase in production/nonsupervisory employees. Contrast that to long-haul general freight truckload, down 2.9% in total jobs and 5.3% among production/nonsupervisory employees.

Not to mention owner-operators

While total trucking payroll employment bottomed out in April 2020, production/nonsupervisory employment in general freight truckload didn’t bottom out until April 2021. At that point, jobs were down 6.2%, which is roughly equal to the total loss in overall trucking employment in March and April 2020. So, with that population still down 5.3%, over-the-road trucking has only begun to recover its pre-pandemic workforce.

On top of that, the employment numbers don’t even consider carriers’ loss of capacity in the form of leased owner-operators. Although we have no comprehensive data on the leased owner-operator population, we can presume that most of the carriers involved in the huge surge in newly authorized trucking companies that began in July 2020 are former leased owner-operators. More than 70% of those carriers have just one driver, and it is much easier for leased operators with their own trucks to strike out on their own than it is for company drivers who must buy trucks in a very hot used-truck market.

So, if you are a truckload carrier struggling to fill trucks and cover your customers’ load tenders, it’s not just you.

For more information visit FTR's website.

This column first appeared in the December 2021 issue of Heavy Duty Trucking.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →