FTR's Trucking Outlook: What the Numbers Say About Freight, Rates, and Drivers

What Do New Small Carriers Mean For Trucking Capacity?

Strong market conditions and extraordinary financial assistance from Washington have sparked an unprecedented surge in the number of newly authorized trucking companies — especially small ones.

by Avery Vise, FTR

December 3, 2021

High spot freight rates, and the availability of apps to easily book freight, have likely fueled the rise in new small fleets.

Source: FTR Analysis of FMCSA MCMIS Data Snapshots from March 2020 and September 2021

3 min to read

For more than a year, strong market conditions and extraordinary financial assistance from Washington, among other factors, have sparked an unprecedented surge in the number of newly authorized trucking companies — especially small ones.

From July 2020 through September 2021, the Federal Motor Carrier Safety Administration approved more than 104,000 new for-hire trucking companies, and that’s excluding private fleets that have added authority. These are huge numbers, but they do not account for the other side of the ledger. Even during periods of robust market conditions like today, many carriers exit the market for a variety of reasons.

To understand how the profile of for-hire trucking has changed during the pandemic, FTR compared a snapshot of data filed with FMCSA as of September 2021 to data filed as of March 2020 for carriers that held operating authority as of those two months. The number of purely for-hire carriers (excluding private fleets with authority) holding authority rose by more than 78,000, or nearly 39%, during the period. The number of one-truck for-hire carriers jumped 52%.

More important than the change in the number of carriers is the change in truck and driver capacity. This analysis is a bit more complicated, because carriers are required to update their profile data only once every two years on a staggered schedule. Therefore, the March 2020 snapshot includes carriers that had not updated their data during the industry’s growth in 2018 and 2019. However, 85% of the carriers in the March 2020 snapshot filed in 2019 or 2020. The staggered reporting also affects the September 2021 snapshot, of course, but two-thirds of carriers have filed this year. So while a comparison is far from precise, it should be a reasonable approximation.

One development that arguably distorts capacity changes is the extraordinary growth in parcel and local delivery during the pandemic. This capacity is an essential part of freight transportation, but these operations — UPS, FedEx, FedEx Ground Package, and Amazon Logistics — are fundamentally different and, arguably, are more competitors for driver capacity than sources of it. Together, those operations added about 11% to their truck fleets and 23% to their driver forces between the two snapshots.

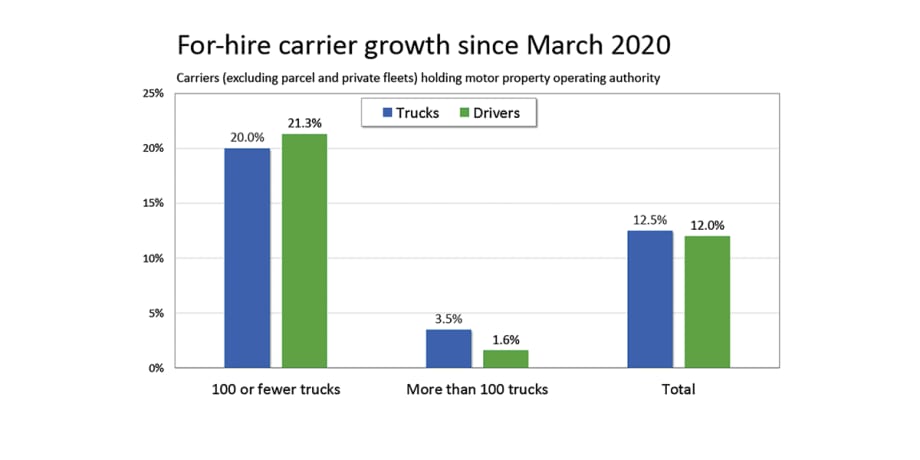

If we exclude the parcel operations, the number of trucks rose 12.5% and the number of drivers increased 12% between the March 2020 and September 2021 snapshots.

For carriers struggling to find enough drivers, these figures might sound preposterous. The comparison probably does overstate the growth somewhat due to the reporting timeframes described above. However, FTR believes that the driver supply issues many truckload carriers face have more to do with supply chain distortions that are keeping spot market volume and rates high than they do with the overall supply of drivers.

Owing to the surge in new entrants, the greatest capacity growth has been among the smallest carriers. But to simplify the discussion, we bundled carriers into two groups: 100 or fewer trucks and more than 100 trucks. Carriers with 100 or fewer trucks saw a 20% increase in truck capacity and a 21.3% increase in driver capacity. Excluding the parcel operations, carriers with more than 100 trucks posted gains of 3.5% in trucks and 1.6% in drivers.

Smaller carriers have increased their market share modestly during the pandemic. Carriers with 100 or fewer trucks now represent about 58% of trucks and 57% of drivers, up from about 55% and 53% previously. This share could grow further if spot rates remain robust, and more fuel could be coming soon owing to the Biden administration’s proposal to require vaccinations or weekly COVID testing for workers at companies with 100 or more trucks.

This column first appeared in the November 2021 issue of Heavy Duty Trucking.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →