The Freight Recession Isn’t Over: Why Trucking’s Recovery Remains Elusive

Tonnage, Trucking Conditions Indexes Show Continued Stagnation

The murky outlook for a recovery in the freight market remains murky, according to industry indexes released this week.

August 21, 2025

Some of the usual economic drivers of truck tonnage were mixed in July, with housing starts and retail sales up, while manufacturing output was flat to down.

Source: ATA

4 min to read

The outlook for a recovery in the freight market remains murky, as the American Trucking Associations says in its latest tonnage index that there’s been no clear trend for truck freight in recent months.

In addition, FTR’s Trucking Conditions Index was the lowest so far this year.

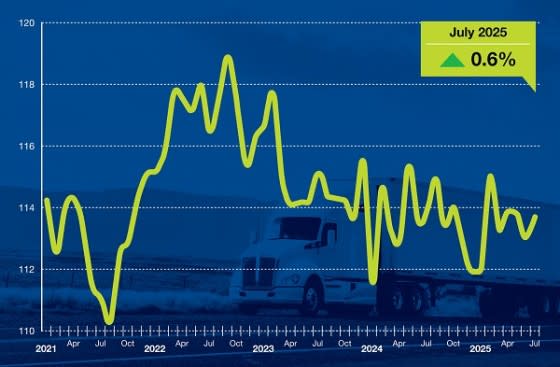

ATA Tonnage Index

Trucking activity in the United States increased slightly in July, but activity has been fairly flat since March, based on ATA’s tonnage numbers.

Specifically, truck freight tonnage rose 0.6% after falling 0.7% in June, according ATA’s advanced seasonally adjusted For-Hire Truck Tonnage Index.

“July truck tonnage increased sequentially, but did not erase the 0.7% decline in June,” said ATA Chief Economist Bob Costello in a news release.

“Since March, truck tonnage has been in a tight range. The good news is truck freight volumes haven’t fallen much over that period, but we are not seeing many increases either.”

Some of the usual economic drivers of truck tonnage were mixed in July, with housing starts and retail sales up, while manufacturing output was flat to down.

In July, the ATA advanced seasonally adjusted For-Hire Truck Tonnage Index equaled 113.7, up from 113.0 in June.

The index, which is based on 2015 as 100, slipped 0.1% from the same month last year after falling 0.4% in June. Year-to-date, compared with the same period in 2024, tonnage was unchanged.

ATA also said June’s seasonally adjusted tonnage index decline was larger than first reported in ATA’s July tonnage report.

The not seasonally adjusted index, which calculates raw changes in tonnage hauled, equaled 116.8 in July, 1.9% above June’s reading of 114.6.

Both indices are dominated by contract freight, as opposed to traditional spot market freight.

The tonnage index is calculated on surveys from ATA’s membership.

Big Swings in FTR’s Trucking Conditions Index

FTR’s TCI swung to -1.83 in June from a strong 3.56 reading in May, which was the strongest since October 2022.

The big drop in June was due primarily to freight rates and fuel prices. The expectation is for trucking conditions to be much closer to neutral during most of the second half of 2025, according to FTR.

The TCI tracks the changes representing five major conditions in the U.S. truck market: freight volumes, freight rates, fleet capacity, fuel prices, and financing costs.

"We still forecast a steadily but only modestly more favorable market for carriers next year,” said Avery Vise, FTR’s vice president of trucking, in a news release.

“However, swings in freight volume and fuel prices — and to a lesser extent, freight rates — continue to generate volatility in trucking conditions.

“Capacity utilization has been the most stable factor, but it has been only marginally beneficial to trucking companies. So far, the economy is weathering tariffs and other stresses better than anticipated, and our latest freight outlook is not as weak as it was previously.

“At least in the near term, though, we still believe forecast risks are weighted more to the downside than the upside.”

Tariff-ying Forecast?

Another trucking and freight analysis company, ACT Research, said in a LinkedIn post that a key takeaway from a market update and forecast on Day 2 of its Market Vitals Seminar was: "In a nutshell, the freight situation is tariff-ying. Carrier profits remain weak. Freight rate traction is nonexistent. Private fleets are pulling back."

And, it said a key takeaway from an economic panel was that the commercial vehicle industry faces an economy currently marked by weaker growth, rising inflation, and slower/unbalanced job gains, coupled with a lengthy freight recession and the early innings of tariff impacts.

Some Good News?

ITS Logistics in its August ITS Supply Chain Report said the trucking sector saw modest expansion in July despite larger global economic uncertainty and rising industry costs.

In addition, the drayage sector experienced the second-highest volume of U.S. imports ever recorded, coming in just 555 TEUs shy of the all-time high in May 2022.

“While capacity has tightened with ongoing carrier exits, the real story is that cost pressures remain significant and freight rates, broadly, are still challenged — just barely covering the bills,” said Josh Allen, Chief Commercial Officer at ITS Logistics, in a news release.

“This isn’t broad-based recovery. The opportunities that exist are selective, shaped by tariff volatility and a shifting regulatory environment.”

Updated 3:40 EDT to add information from ACT Research and ITS Logistics.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →