J.B. Hunt 1st Quarter Earnings Miss Expectations

Bad weather, higher costs for driver pay, and pressure on rates as capacity loosens were all factors in J.B. Hunt Transport Services’ disappointing first-quarter earnings.

J.B. Hunt's Final Mile Services saw an increase in revenue of $26 million compared to first quarter 2018, but it also had higher network facilities costs.

Photo by Deborah Lockridge

Bad weather, higher driver costs, and pressure on rates as capacity loosens were all factors in J.B. Hunt Transport Services’ disappointing first-quarter earnings.

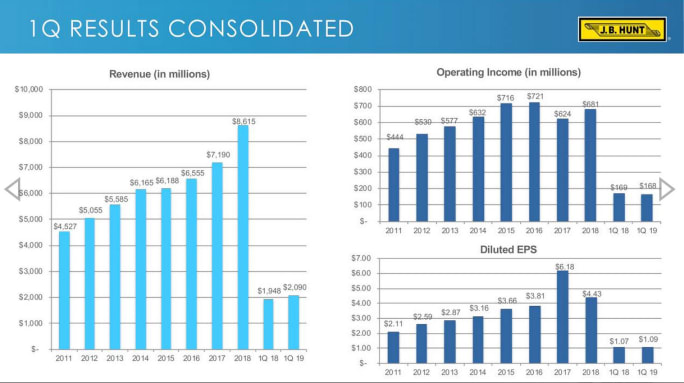

J.B. Hunt revenue was $2.09 billion, up 7% from the same time a year ago, but lower than the 2.2 billion expected. Operating income of $168 million was down 1% and significantly short of the $196 million expected. And earnings per share of $1.09 were higher than last year’s $1.07, but fell short of the $1.25 expected. Net earnings of $119.6 million was up slightly from last year’s $118.1 million.

“The published results obviously revealed headwinds in parts of our business that masked improvements and forward progress in others,” said David Mee, chief financial officer, in an earnings call with investors.

Benefits from higher customer rates and new customer contracts were offset by:

• increased rail purchased transportation costs;

• lower intermodal network utilization;

• lower productivity in winter weather affected regions;

• higher driver and non-driver salaries, wages and benefits;

• higher Final Mile Services (FMS) network facilities costs;

• increased technology spend on the J.B. Hunt 360° platform and legacy system upgrades;

• increased equipment ownership and maintenance costs.

Intermodal

“In Intermodal, volume or lack thereof is obviously the main story,” Mee said. “We expected it to be down from a recently strong first quarter 2018 due the expected and planned rail closings and train reroutings and from our sequential volume trends coming off a very strong pricing season in 2018.

“The service disruptions from weather issues starting in late January and progressing through late February actually caused some freight to divert back to the highway in addition to loads being outright cancelled.

“When the service began to improve, we did not see a snapback in customer demand in March, which was our biggest surprise and frankly our miss to our expectations. While it is way too early to make a trend call for even second quarter 2019 or for the rest of the year, we are still waiting for customer demand to accelerate.”

Intermodal revenue per load excluding fuel surcharges increased approximately 11% over first quarter 2018 levels, but there was a 7% decline in volumes.

Dedicated and Final Mile

Dedicated Contract Services (DCS) segment revenue increased by 22% over a year earlier, thanks to both new customer contracts and customer rate increases. Included in the DCS revenue growth, Final Mile Services (FMS) recorded an increase in revenue of $26 million compared to first quarter 2018.

Operating income increased 24% from a year ago, primarily from increased productivity and additional trucks under new customer contracts, partially offset by higher facilities rent and costs to expand the FMS network, increased driver wages and higher recruiting costs, including the length of time to fill open trucks in certain geographic regions.

A net additional 1,644 revenue-producing trucks (440 of those added compared to the fourth quarter 2018) were in the fleet by the end of the quarter compared to prior year. Approximately 41% of these additions represent private fleet conversions and 9% represent FMS vs. traditional dedicated capacity fleets. Customer retention rates remain above 98%.

“DCS did have a progressive quarter, as they successfully onboarded an additional 400 plus trucks into new customer contracts and began the integration of the Cory acquisition which closed in February,” Mee said. (J.B. Hunt bought Cory 1st Choice Home Delivery in January.)

Brokerage and Logistics

Integrated Capacity Solutions (ICS), which provides non-asset, asset-light, traditional freight brokerage and transportation logistics solutions, saw load growth of 15%, but there was a 12% decrease in revenue per load over the same period in 2018.

“ICS results demonstrated the aggressive customer pricing becoming apparent in a brokerage market,” Mee explained, “the adequate supply of capacity to meet that customer demand, and our commitment to devote resources to further develop the technology expected to capture additional revenue opportunities, assist driving out waste in the transportation industry, and lower our enterprise operating costs.”

In addition to its reported revenue, he pointed out, ICS sold approximately $80 million in revenue recognized by J.B. Hunt’s other business units, especially in intermodal.

When asked about the pricing issue in ICS, Shelley Simpson – executive vice president, chief commercial officer, responded, “I would say just in general the brokerage market is competitive. This season has been very aggressive.” She also cited “new competitors in this space, specifically on the digital freight-matching side.”

What stood out was the success of the Marketplace for J.B. Hunt 360, an online marketplace for shippers and carriers. Mee said volume through the platform was up over 100% year-over-year, which yielded a 92% increase in revenue executed, increasing to $186 million in the first quarter 2019, vs. $96 million in the same period last year.

Truck

In the Truck segment, revenue increased 10% compared to a year ago, to $102 million, primarily from customer rate increases and a larger operating fleet. Operating income was $7 million, up 41%.

Revenue excluding fuel surcharge increased approximately 12% from first quarter 2018, primarily from customer rate increases and a 4% increase in load count. Volume was negatively impacted by the weather in the Midwest region. Revenue per load excluding fuel surcharge increased 8%, primarily from a 12% increase in rates per loaded mile and a 4% decrease in length of haul. At the end of the first quarter, JBT operated 2,043 tractors, up from 1,926 the same time a year ago.

“Truck continued to focus on its return on invested capital profile, as was evident by the change in its capacity composition from a roughly 65% owned equipment in first quarter of 2018 to roughly 50% owned equipment in first quarter 2019 and continued rationalization of its trailing fleet to fit actual customer demand,” Mee said.

However, benefits from the higher revenue per load and lower equipment ownership costs were partially offset by higher driver and independent contractor costs per mile and higher recruiting costs per driver and independent contractor compared to first quarter 2018.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →