Growth in Truck Freight, Rates to be Slight in 2020: FTR

Barring the unexpected, trucking can generally expect flat to moderate growth in demand and rates in 2020, with most of the growth in the second half of the year.

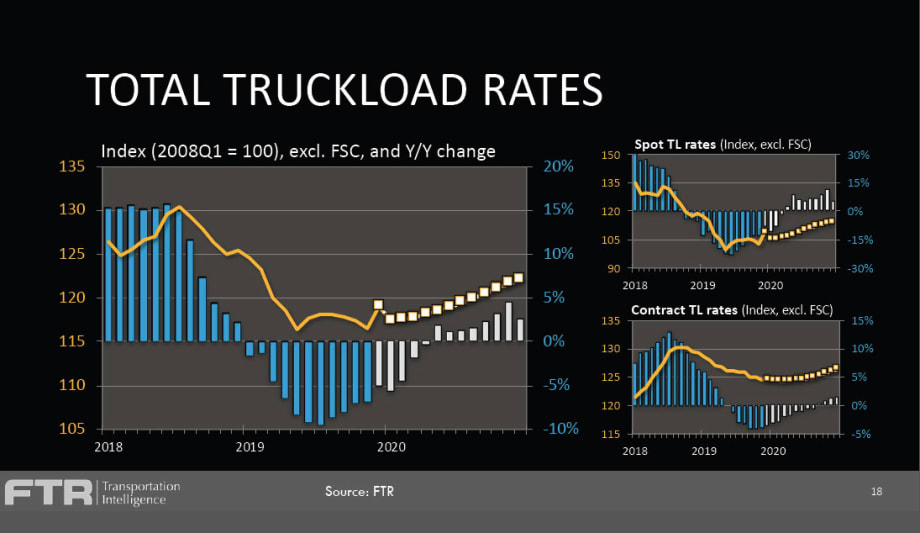

FTR's truckload rate forecast for 2020 is for slight growth.

Graph courtesy FTR

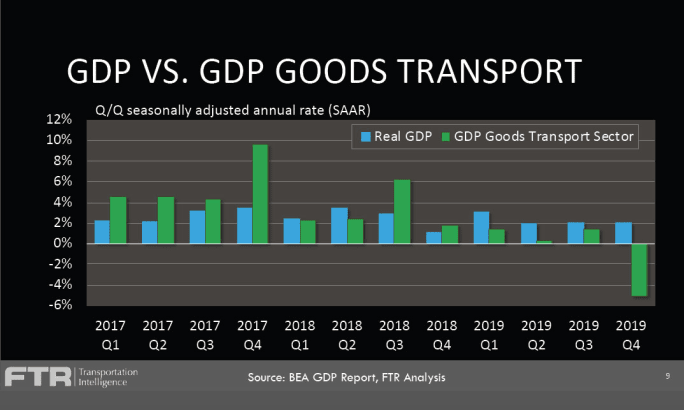

What FTR calls the Goods Transport Sector, the portions of GDP that affect truck freight, performed vastly differently from overall GDP in the last few quarters.

Graph courtesy FTR

Barring the unexpected, trucking can generally expect flat to moderate growth in demand and rates in 2020, with most of the growth in the second half of the year. That’s the takeaway from FTR Associates’ Outlook for Trucking webinar on Feb. 13.

Avery Vise, FTR vice president, trucking, noted that freight-related economic indicators are mixed:

Manufacturing: The ISM index in January rebounded from several months in the negative to basically flat, as orders for durable and core capital goods are basically flat.

Construction: Total construction spending has risen since June and was higher year over year in October and November, while housing starts in December were the highest since 2006.

Housing: Sales of new homes are highest since 2007 and existing home sales are the strongest in nearly two years, while mortgate rates are near all-time lows.

Consumer: Retail sales were at an all-time high in December

Inventories: The inventory-to-sales ratio finally dipped in November, but it had been stuck at its highest level since late 2016. However, Vise noted, e-commerce could be changing views on what this metric should be.

Employment: Payroll job growth has accelerated since mid 2019 and exceeds the average during the recovery, while unemployment is near a 50-year low and wage growth is solid.

Trade: Total U.S. trade in goods was down slightly in 2019, but trade is suffering from global issues, from the U.S. trade war with China to the Coronavirus outbreak. The U.S. Mexico-Canada Agreement, which replaces NAFTA, and the Phase One deal with China should help stabilize the environment, but what will happen with the virus is impossible to predict.

Trucking-Specific Indicators

Turning to more trucking-specific indicators, Vise said FTR’s overall forecast for truck loadings for 2020 is 0.7% growth over the course of the year. “That’s not very much, certainly not from the perspective of for-hire carriers, to stimulate rate growth.” Refrigerated freight will be the clear leader in freight volume this year, he said.

The rate environment so far is trending a little above flat for the year, Vise said. FTR projects the truckload market will see about a 0.4% increase in rates over the course of the year. “We’re in a negative environment now and will get stronger in the second half of the year.” The growth is mostly expected to come from the spot market, offsetting a continued slight decline in contract rates. Again, refrigerated freight is expected to outpace the rest of the industry given the expected growth in volume, and FTR is projecting a 2.5% increased in rates for the year – but flatbed and specialized rates will see a “mildly negative environment,” probably dropping, but by less than 1%.

Of course, demand is only part of the factor in rates; the other is capacity. There are a lot of ways to look at capacity, but Vise used for-hire trucking jobs as a proxy, because the majority of those jobs are drivers, and the majority of capacity. Movement is driven by driver supply. That number has been pretty much flat for the last five months, he said, down 0.4% from an all-time high last July. “Moving forward, we would not expect to see too much growth and possibly some modest losses,” he said.

Trucking Capacity Factors

Several trucking issues may affect capacity this year, Vise said.

Rapidly rising insurance costs, he said, have been a major factor in an above-trend number of carriers losing operating authority over the last five quarters. The latest operating costs survey from the American Transportation Research Institute, which covered costs in 2018, indicated insurance premiums as measured by marginal cost per mile rose 12% in 2018 over 2017, significantly outpacing other operating costs. “Anecdotally, we understand 2019 was much more painful,” Vise said. It’s particularly a problem for smaller carriers, which saw increases in the neighborhood of 50% from 2017 to 2018 when measured in marginal cost per mile, according to ATRI.

Other issues that could affect capacity, utilization, and productivity, and therefore rates, include the final transition to electronic logging devices under the ELD mandate that went into effect in December; and the new drug and alcohol clearinghouse that went into effect in January, along with a rise in the random test rate to 50%.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →