Related: Capacity is Catching up to Demand in ACT’s For Hire Trucking Index

Can Carriers Hire Enough Drivers to Support Booming Truck Orders?

A strong September meant that North American Class 8 net orders set another record in the third quarter of 2018, breaking the record set in the first quarter of the year. FTR says it often faces skepticism about how fleets can possibly fill these trucks.

by Avery Vise, FTR

October 22, 2018

3 min to read

A strong September meant that North American Class 8 orders set another record in the third quarter of 2018, breaking the record set in the first quarter of the year. Orders totaled 146,000. Monthly order volume was the 10th highest of all time in September, and yet the month represented only the fifth best month this year.

FTR often faces skepticism about how fleets can possibly fill these trucks given a severe driver shortage and a national unemployment rate of 3.7% – the lowest in 49 years. It’s a fair question, but when we break down all the elements, it’s not as daunting as it might appear.

Let’s start with the fundamental point that a truck order is not a sale. Orders placed today can be cancelled tomorrow, next week or indeed – given current backlogs – well into 2019. However, while cancellations are to be expected, based on our current forecast we do not anticipate anything out of the ordinary. Also, some of these orders will end up, initially at least, in dealer stock rather than in fleet operations. And even among trucks actually sold to fleets, many will just replace existing units. As the North American truck fleet grows to handle more freight, more trucks must be replaced in any given trade cycle. Even so, the 2018 order activity clearly implies growth, and growth requires more drivers.

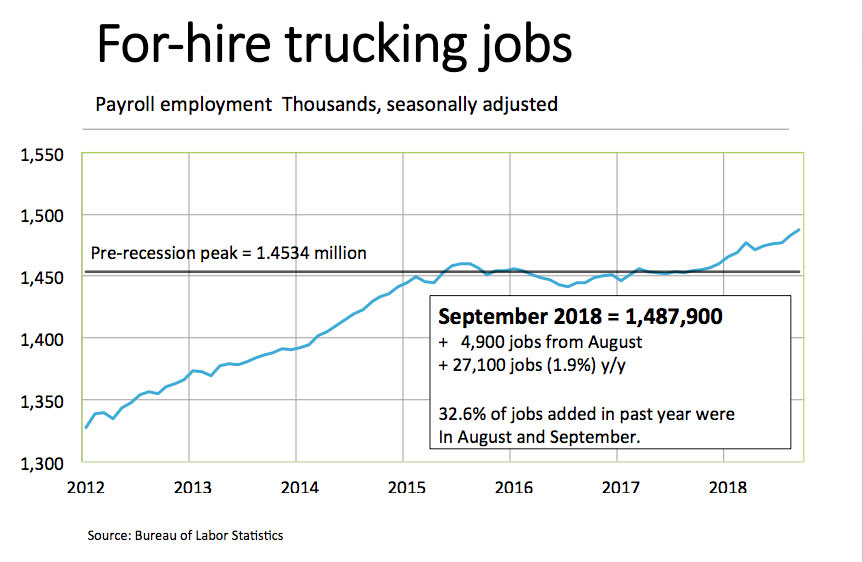

FTR estimates that 105,000 more drivers would be needed in 2019 to fill the Class 8 trucks we expect to be sold over and above replacement demand. That might sound like a big number, but it’s just over 3% of the current Class 8 driver force, which FTR estimates at 3.37 million. Payroll job growth in for-hire trucking currently is running above 2%. For-hire carriers added 4,900 payroll jobs in September on top of 5,900 added in August, according to preliminary data from the Bureau of Labor Statistics. That’s just under one third of the 33,100 jobs added since September 2017. So even as the overall job market has tightened, trucking companies’ hiring has accelerated. Not all those jobs are driving, of course, but most certainly are.

Also, 33,100 jobs added in a year is hardly pushing the limit if history is any guide. On a year-over-year (y/y) basis, the industry was adding more payroll jobs than that every month from June 2014 through August 2015. For example, the y/y increase in February 2015 was 55,200 – a 4% increase. And while the month-over-month (m/m) increase in September was solid, at least based on preliminary figures, we saw higher m/m increases in 23 months since 2010, including three months in 2018. So even with a low unemployment rate, continued growth seems feasible, especially given solid pay increases this year.

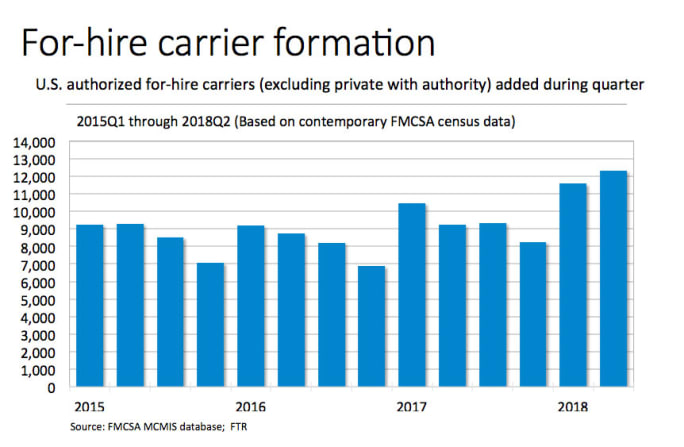

Not all driving jobs show up in the payroll figures for for-hire trucking, however. The biggest omission is what is happening with private fleets. Other significant blind spots in BLS numbers are leased and independent owner-operators. This segment is harder to assess, but available data suggests we are seeing growth. For example, FTR’s analysis of newly authorized for-hire carriers – most of which we would classify as independent owner-operators – shows a surge of new carriers in the first half of 2018. Given the strength in freight demand and rates, this isn’t surprising. As more used equipment becomes available in the coming months both on the open market and internally at carriers through lease-purchase programs, we likely will see continued strong growth in owner-operators. Because most new owner-operators naturally come from the ranks of company drivers, carriers’ solid growth in payroll job growth means that overall driver capacity is even higher.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →