While final economic numbers for 2017 have yet to roll in, economic growth was strong. Will it keep moving higher into the New Year?

While final economic numbers for 2017 have yet to roll in, economic growth was strong. Will it keep moving higher into the New Year? Analysis by Business Contributing Editor Evan Lockridge.

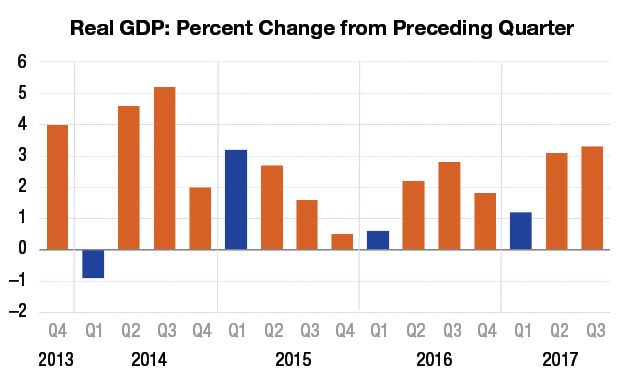

Source: U.S. Commerce Department Bureau of Economic Analysis

While final economic numbers for 2017 have yet to roll in, economic growth was strong. Will it keep moving higher into the New Year?

The broadest measure of the economy, the nation’s gross domestic product, grew at an annual rate of 3.3% in the third quarter, according to a Commerce Department estimate released in late November. (A revised estimate was some two weeks away at press time.)

That followed 3.1% annualized GDP growth in the second quarter, marking the first time this total measure of the output of goods and services increased 3% or more for two straight quarters since 2014.

Many economists predict things will remain strong once fourth quarter and full-year 2017 numbers are reported, with projected improvements of around 2.7% and 2.2%, respectively. That would still be far off the pace of the halcyon days before the Great Recession, but par for the course since the end of the financial crisis. But can the economy ever do better? Perhaps.

The problem continues to be that pesky first quarter of the year. In 2017, first quarter GDP growth was 1.2%. In the first quarter of 2016 it was just 0.6%. And in the first quarter of 2014, it dropped at a near 1% annual rate. In all three cases it was the lowest GDP reading of the year (unless the final quarter of 2017 becomes a total surprise). In contrast, in 2015, the first quarter had the best GDP performance of the year’s four quarters. And in 2012 and 2013 the first quarter performed near or at the top for each of those years.

The point is that the first quarter of the year is a volatile time. From snowstorms that paralyze freight movements and keep consumers out of stores, to labor disruptions and other factors, the first three months of the year can be a wild ride.

As of press time in mid-December, many economists were predicting first quarter 2018 GDP growth to be in the neighborhood of 2.4%. For the full year, the independent research group The Conference Board and the Federal Reserve forecast total 2018 GDP growth of 2.5%. While that’s below the 2.9% and 2.6% annual rates seen in 2016 and 2015, it still would represent one of the best two-year runs since before the Great Recession.

Good fundamentals are behind the projections. Business investment improved in 2017 after falling the year before, while unemployment is ultra-low. Manufacturing has been on an upswing along with consumer optimism, though both at press time were down a bit from their fall peaks. And housing has more bright spots than dim ones. In other words, more cylinders in the economic engine are more evenly firing.

For trucking, a combination of the strong economy, combined with capacity pressure from hurricane recovery and the ELD mandate, is creating a very tight market and rising freight rates for carriers. Whether that carries through the first quarter depends on how mandatory ELD implementation and enforcement is going, along with the usual uncertainties of severe winter weather and other first-quarter surprises.

An expanded Trucker Path and Truckstop.com integration brings more freight opportunities into the TruckLoads app while emphasizing security and network quality.

Read More →

Strong March freight demand combined with a spike in fuel costs pushed both spot and contract truckload rates to their highest levels in more than two years.

Read More →

Everyone’s talking about AI — but is your transportation management system actually built for it?

Read More →

Being part of KTG will allow Sharp to expand and improve its services.

Read More →

The Fair Compensation for Truck Crash Victims Act would increase insurance requirements for interstate motor carriers by nearly seven times.

Read More →

Strong freight rates push TCI to 10.2, but FTR expects fuel-price volatility to skew March results.

Read More →

C.H. Robinson is waiving fees on fuel cards and cash advances for April and May, aiming to help carriers offset rising diesel costs tied to geopolitical instability.

Read More →

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

After years of steady, methodical progress, Peter Voorhoeve says the OEM’s latest lineup isn’t just evolutionary. It’s delivering real, measurable gains for fleets right now.

Read More →

BeyondTrucks says its new RateAgents can turn plain-language rate logic into working code, starting with fuel surcharges — a critical but notoriously complex piece of carrier revenue.

Read More →