When shopping for commercial auto insurance, it’s important to consider a number of factors, not just cost.

by Bill Caudill

December 9, 2014

3 min to read

When shopping for commercial auto insurance, it’s important to consider a number of factors, not just cost. Compare offerings and find out which insurer will best fit your business needs. Here a few things to keep in mind that will help you make the most informed decision.

Ad Loading...

Claims

Ad Loading...

Find out if they have specialized claims reps. If you do have an accident, it’s important to find a company that has dedicated commercial auto claims representatives, not general reps who work for a third-party. Specialized claims reps will help get you back on the road quicker. Ask if they have dedicated repair shops. Similar to specialized claims representatives, finding an insurer with a network of shops is important. In addition to speeding up the repair of your vehicles, many of these shops will offer guarantees on their work for long periods of time. That offers you peace of mind when you pick your truck up and put it back in commission.

Service and Coverage

Make sure their coverages fit your needs. Every business is different, which means business owners have different coverage needs. Ask about the things you and your business need to be covered, and be specific. For example, if your truck is paramount to getting supplies to your customers, check if your insurer offers rental vehicle coverage. It provides you with a temporary vehicle if yours is out of service.

Look for experience in your trade. Ask around and do your research to see if the insurer has a history of handling trucking claims. A proven track record with your trade is a good indicator of how well an insurer will handle your claim if you ever need to file one. If you can’t find the information you’re looking for, don’t be afraid to ask about their experience.

Ask if they’re available 24/7. Chances are you don’t work a typical 9-5 schedule, so look for an insurer that can work around your timeline. You never know when you’ll need your insurance company to be there for you. Find a company that works around your schedule, not vice-versa. And 24/7 doesn’t just apply to call centers and claims representatives – check if your insurer has coverages like Rental Reimbursement with Downtime, which will compensate you for lost time and help find you a replacement vehicle while your rig is being fixed.

Ad Loading...

Pricing

Value doesn’t always mean price. Make side-by-side comparisons and see who’s giving you the most for your money. Consider other factors like bundling packages, customer service and special offers. Then, once you’re comfortable with what your insurer is covering, ask about discounts.Look at the discounts. After you’ve taken the time to compare the value of what you’re getting, check what discounts you’re eligible to receive. There are many kinds of discounts, including discounts for having at least three years of business experience, paying your policy in full and having a valid commercial driver’s license. You might even be able to get a discount for something as simple as showing proof of prior insurance coverage. Ask your insurer or independent agent plenty of questions to ensure you’re getting the most for your money.

Bill Caudill is a commercial auto product manager at Progressive.

This article was authored under the guidance and editorial standards of HDT's editors to provide useful information to our readers.

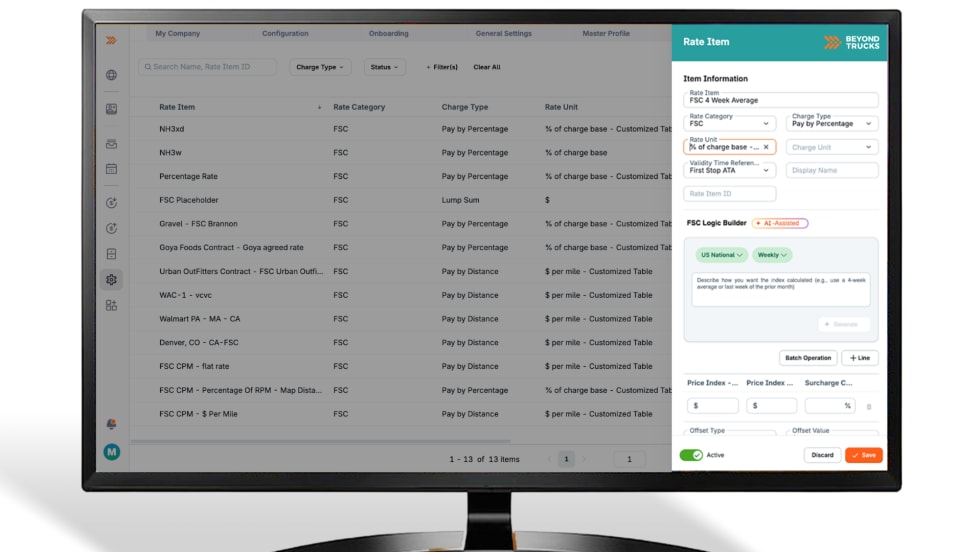

BeyondTrucks says its new RateAgents can turn plain-language rate logic into working code, starting with fuel surcharges — a critical but notoriously complex piece of carrier revenue.

Soft freight conditions persist, but aging fleets, strong order intake, and new-product momentum signal a more optimistic second half of 2026, Volvo Trucks North America says.

Cargo theft is evolving from regional smash-and-grab operations to sophisticated fraud schemes. Strategic theft now accounts for roughly a third of cargo crime, with incidents rising sharply in recent years. Here’s how the schemes work — and what fleets can do to protect themselves.

Heavy Duty Trucking's Top 20 Products awards recognize the best new products and technologies. Check out the award presentations at the 2026 Technology & Maintenance Council annual meeting.

The Detroit® Gen 6 engine platform proves that real progress doesn’t require a complete redesign. Built on 20 years of trusted technology, these engines are designed for efficiency, stronger performance, and greater reliability than before. And they do it all while complying with 2027 EPA standards on every mile.

The 2026 ACT Expo is focusing heavily on what organizer Erik Neandross calls trucking's digital frontier. This interview excerpt dives into artificial intelligence, zero-emission vehicles, and tips to make sense of it all.

There's an amazing amount of new technology for trucking out there. For fleets, the challenge is figuring out what’s real, what’s hype, and what’s worth investing in.

Artificial intelligence, the software-defined vehicle, telematics, autonomous trucks, electric trucks and alternative fuels, and more in this HDT Talks Trucking interview

ACT Research data shows volumes hitting a four-year high and supply-demand balance strengthening, but higher oil prices are undercutting tariff relief and tempering optimism.

The patent-pending cargo solution integrates a digitally connected cargo door and an intelligent locking system with the TrailerHawk.AI technology platform.