Spot Truckload Market Volume Jumps, Rates Move Higher

The availability of spot truckload freight gained 4.8% and the number of trucks posted slipped 3.2%, while rates remained unseasonably high, for the week ending Nov. 4, according to DAT Solutions and its network of load boards.

The availability of spot truckload freight gained 4.8% and the number of trucks posted slipped 3.2%, while rates remained unseasonably high, for the week ending Nov. 4, according to DAT Solutions and its network of load boards.

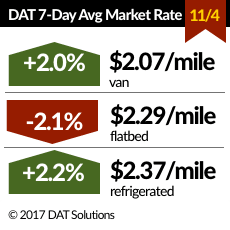

National average spot van and reefer rates jumped after receding for three straight weeks while the flatbed rate declined after two months of steady increases. However, national average spot rates remain above seasonal norms:

Van: $2.07 mile, up 4 cents from last week

Flatbed: $2.34 per mile, down 5 cents from the week before

Reefer: $2.36 per mile, up 5 cents from the previous week

(All rates cited include fuel surcharges.)

The number of van load posts increased 7% as retail freight enters the truckload distribution pipeline. Combined with a 4% decline in the number of trucks posted, this sent the van load-to-truck ratio up from 5.9 to 6.3 van loads per truck.

The van ratio has declined since hitting a peak of 7.0 loads per truck during the final week in September but is more than double what it was last year at this time.

Tighter capacity pushed spot market van rates higher across much of the country, as average outbound prices rose on 58 of the top 100 van lanes. Los Angeles remained the number one market for van load volume where the average outbound rate gained 11 cents to $2.49 per mile last week.

With holiday goods moving through the cold chain, the number of spot reefer load posts increased 18% last week. The reefer load-to-truck ratio increased from 9.7 to 11.8 loads per truck as available capacity fell 3%.

Of the top 72 reefer lanes, 39 had rising rates. Among the markets showing strength over the past week:

Green Bay, $3.72 per mile, up 12 cents

Chicago, $3.33 per mile, up 14 cents

Elizabeth, New Jersey, $2.20 per mile, up 6 cents

Los Angeles, $2.73 per mile, unchanged

Rebuilding efforts in Florida and the rest of the Gulf Coast have put tremendous pressure on flatbeds lately. Compared to September, flatbed load posts were up 5% in October while truck posts climbed 12%. That resulted in a 6% decline in the load-to-truck ratio compared to the previous month's spike. At 39.5 loads per truck, the ratio last month was 172% higher than in October 2016.

The national average price of on-highway diesel during this time ticked upward to $2.88 per gallon, the highest level since June 2015.

With spot freight rates being unseasonably higher than normal, this naturally begs one question: how much longer will rates stay this high?

“It could be a couple more months, at least,” said the latest DAT Blog. “Retail freight is expected to be more plentiful this year, and port traffic is way up. With the ELD mandate coming in December, it seems likely that prices will stay above normal for a while. Demand usually tapers off in February, so rates could slip lower then, until activity picks up again in the spring.”

More Fleet Management

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange connects heavy-duty trucking fleet managers with industry suppliers through one-on-one meetings, small-group discussions, educational sessions, and networking opportunities with both suppliers and other fleet managers.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →

Volvo Trucks Adds Unattended Over-the-Air Software Update Capabilities

The latest evolution of Volvo’s over-the-air update technology allows software updates to run while trucks are parked, helping fleets keep vehicles current without disrupting operations.

Read More →

How Waste Connections is Using Data, Telematics, and AI

How do you manage and maintain more than 18,000 connected trucks? Data. Lots of it.

Read More →

Why Fleet Data Matters More Than Ever at Waste Connections [Watch]

Waste Connections' Chuck Palmer explains how telematics, predictive maintenance, safety analytics, and AI help keep vehicles on the road and drivers safe in this episode of HDT Talks Trucking.

Read More →

NMFTA Launches Free, Anonymous Cybersecurity Threat Report Portal

Organizations are encouraged to anonymously report freight fraud, cargo crime, and cyber threats while gaining visibility into incidents reported across the transportation sector.

Read More →

AI Can Optimize a Fleet. Can It Replace Human Judgment?

Fleets fear falling behind if they don’t adopt AI quickly enough. They also fear what happens if the technology makes the wrong decision.

Read More →

Jamie Hagen Gets Real About Running a Small Fleet in an Uncertain Economy

Small fleet owner Jamie Hagen says new legal risks, volatile fuel prices, and a changing freight market are forcing small carriers to rethink how they operate — and what they can afford.

Read More →