6 Takeaways from Third-Quarter Earnings Reports

Some of the key observations that came out of the earnings reports:

3Q/4Q freight volumes will lack the normal peak season and holiday boost, but not because of weak demand. While consumer spending has been slowing, the real culprit here is high inventories. Shippers are adamant that this is not a read into 2023 at this time.

Capex budgets are being reduced, but not because of weaker profit margins. Rather, improving but continued OEM equipment delays are keeping most companies on allocations into 2023, and are pushing capital expense numbers from 2022 into 2023.

Spot truck rates and ocean container rates have round-tripped to pre-pandemic levels. The driver in the trucking market is a shift of spot freight back to contract markets. Ocean rates are seeing improved port congestion and high inventory levels, resulting in blank sailings and faster sailing times to the West Coast.

Rail network fluidity is improving. While 3Q averages remain subdued, end-of-quarter speed improved about 10% for the industry, and dwell times were approaching double-digit improvements as well.

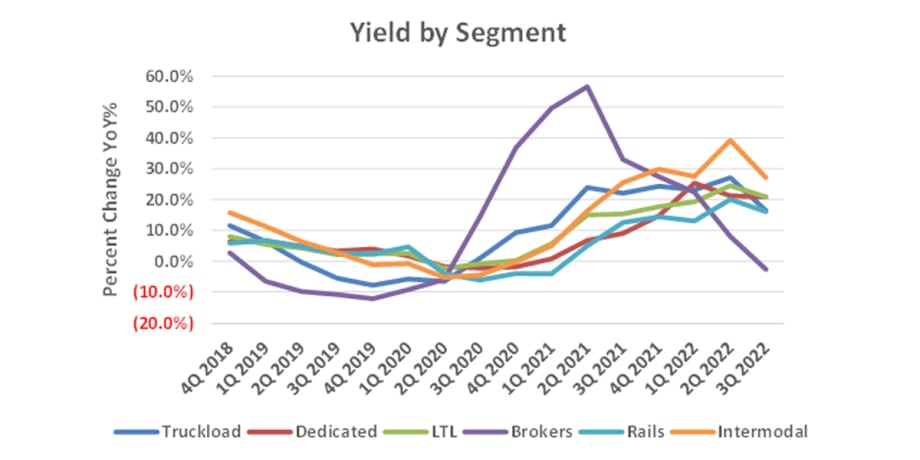

Contract truck pricing could be nearing an inflection point. Truck spot rates have leveled off near 2018 levels, but contract rates remain elevated. However, the second derivative of pricing appears to be turning, and we look for lower growth rates ahead as customers re-bid larger pieces of their networks in 2023.

The over-earnings party continues for used truck equipment. Dealership inventories remain lean and used equipment prices have come down off their peak, but used trucks remain in strong demand. Ryder’s 83% utilization remains near record levels.