“Driver availability no longer is the key issue to watch in trucking conditions.”

Mixed Numbers on Trucking Conditions

FTR's Trucking Conditions Index from April and the Cass Transportation Indexes for May identify trends such as job growth and economic conditions that could point to a weakening after a nearly two-year cycle of surging freight volumes.

June 20, 2022

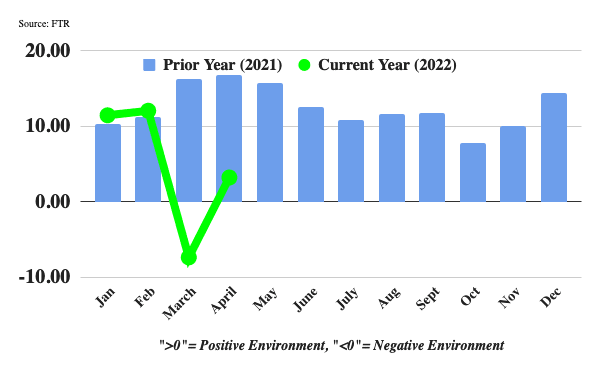

April's trucking conditions bounced back from a dismal March, but are still well below last year.

Source: FTR

4 min to read

FTR's Trucking Conditions Index from April and the Cass Transportation Indexes for May both identify trends such as job growth and economic conditions that could point to a weakening after a nearly two-year cycle of surging freight volumes.

The Trucking Conditions Index rebounded to a reading of 3.21 from March when the index fell to -7.38. However, the April reading otherwise was weak — the lowest since July 2020, not counting March’s negative reading.

The TCI tracks the changes representing five major conditions in the U.S. truck market: freight volumes, freight rates, fleet capacity, fuel prices, and financing costs. The individual metrics are combined into a single index indicating the industry’s overall health.

Diesel prices in April were relatively stable, FTR pointed out, "but softer capacity utilization and freight rates made for positive but lackluster market conditions for trucking companies," it said in a news release.

The outlook is mildly positive in the near term, but ongoing fuel price increases and other factors could result in further negative readings, according to the transportation research firm.

“Recent strong gains in trucking’s payroll employment support our analysis that freight demand has remained solid and that weaker spot market metrics this year indicate a shift of activity back to more normal route guides,” said Avery Vise, FTR’s vice president of trucking. “Driver availability no longer is the key issue to watch in trucking conditions; increasingly, the principal question will be the resilience of freight demand. Downside risks are high and growing due to inflation and related stresses, but our forecasting model so far is not identifying a downturn.”

ACT Research: Turbulent Environment

ACT Research still believes a soft landing is the U.S. economy’s most likely path, but "the potential for a mild recession is becoming an increasingly compelling alternative," according to its latest North American Commercial Vehicle Outlook.

“We find ourselves in a turbulent environment, where still significant positive and increasingly negative economic forces are crashing into one another," said Kenny Vieth, ACT’s president and senior analyst. "With inflationary shocks emanating from Ukraine, the Fed’s task of engineering a soft landing has become increasingly challenging.”

ACT believes downward pressures are building and the probability of recession continues to grow.

“With the current head of steam that includes healthy consumer and business balance sheets, strong employment demand, and pent-up manufacturing sector activity, this inflation-driven economic slowdown is on one hand somewhat unique," Vieth explained. "On the other, traditional recession predictors are in play: Fed rate hikes, high energy prices, negative exogenous events, and falling equity valuations come to mind.”

Cass Freight Index

Looking at its May data, Cass Information Systems says after a nearly two-year cycle of surging freight volumes, two key drivers of growth for the freight cycle — goods consumption and inventory restocking — are faltering.

Combined with a major improvement in driver availability (27,300 new jobs added in the past two months), all signs continue to point to a change in the trajectory of rates in the coming months.

The Cass Transportation Indexes measure changes in North American freight activity and costs based on $37 billion in paid freight expenses for the Cass customer base of hundreds of large shippers.

The shipments component of the Cass Freight Index rose 5.4% m/m in May (up 4% seasonally adjusted), more than recovering the 2.6% decline in April. Normal seasonality would see that rise 2% year over year in June and flat to up 1% for 2022. "The news from the retail sector and in the oil markets suggest that’s probably optimistic, but at this point, it’s a pretty stable environment," Cass said, with no sign of a major downturn.

A simple calculation of the Cass Freight Index data (expenditures divided by shipments) produces a data set of inferred freight rates that explains the overall movement in rates (specifically, the cost of a shipment).

Source: Cass Information Systems

Cass Inferred Freight Rates fell 9.5% m/m on a seasonally adjusted basis in May.

“It’s tempting to see this as a sign that freight costs have peaked, and on a year-over-year basis that is true, as inferred rates will slow all the way to 13% year-over-year in June on normal seasonality," Cass said. "Supply/demand fundamentals have certainly turned looser this year, so it wouldn’t be an unreasonable conclusion. However... the drop was largely due to mix [less-than-truckload vs. truckload], and with fuel prices still adding upward pressure, the descent is not straightforward.”

The 15% year-over-year decline in rates (excluding fuel surcharges) in the more real-time spot markets in early June portends a downcycle on the horizon, according to Cass.

This year has seen a big improvement in driver availability and a flattening of freight demand, which means freight rates will drop, Cass predicted — though it will take several months to filter from the spot market into contract rates.

However, equipment capacity remains limited and could tighten further if the Russia/Ukraine war or China lockdowns worsen the chip shortage.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →