September Trucking Conditions Still Strong

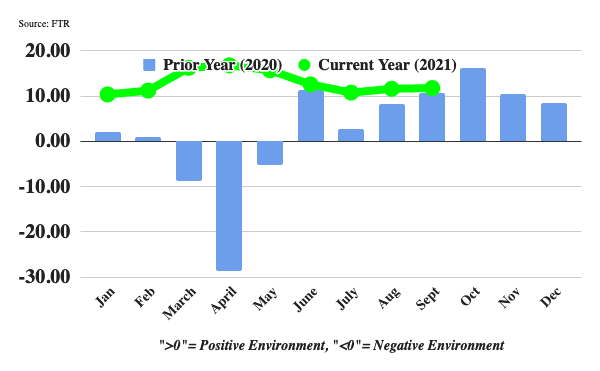

Freight rates continued to strengthen in September, but freight volume and capacity utilization numbers were weaker, according to FTR’s Trucking Conditions Index.

Credit: FTR

Freight rates continued to strengthen in September, but freight volume and capacity utilization were not as beneficial to carriers as they were in July and August, according to FTR’s Trucking Conditions Index.

The September TCI increased marginally to 11.79 from 11.63 in August. FTR’s forecast remains for strong positive TCI readings well into 2022.

“The market remains stubbornly favorable to carriers, due in large part to continued strong consumer spending and the effects of supply chain troubles on productivity,” said Avery Vise, FTR’s vice president of trucking. “The latest payroll employment data for trucking implies a considerably stronger recovery in driver capacity than had appeared previously, but the ongoing surge in newly authorized small carriers continues to shift capacity and thwart a return to normal."

About those employment numbers: Vise told HDT that total trucking employment in September was 1.1% below February 2020, but production/nonsupervisory employee jobs were down 2.3%. This implies that drivers are a drag on trucking’s recovery, not a contributor to it. With one exception, all segments of trucking in the BLS data are down. The one major exception is local general freight trucking, which has seen a 5.2% increase in total payroll employees and a 7% increase in production/nonsupervisory employees. On the other hand, long-haul general freight truckload is down 2.9% in total jobs and 5.3% among production/nonsupervisory employees.

So while those payroll employment numbers look good on the surface, a deeper dive indicates what the trucking industry already knows, that long-haul trucking is having a hard time finding drivers.

“Even if carriers start to see recruiting challenges ease up, continued struggles in truck production due to parts and material shortages could limit capacity in the months ahead," Vise said. "A key factor for the freight market will be whether consumer spending remains so robust beyond the holidays and the end of advance child tax credit payments in December.”

The TCI tracks the changes representing five major conditions in the U.S. truck market: freight volumes, freight rates, fleet capacity, fuel price, and financing. The individual metrics are combined into a single index indicating the industry’s overall health. A positive score represents good, optimistic conditions. Conversely, a negative score represents bad, pessimistic conditions. Readings near zero are consistent with a neutral operating environment, and double-digit readings in either direction suggest significant operating changes are likely.

More Fleet Management

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

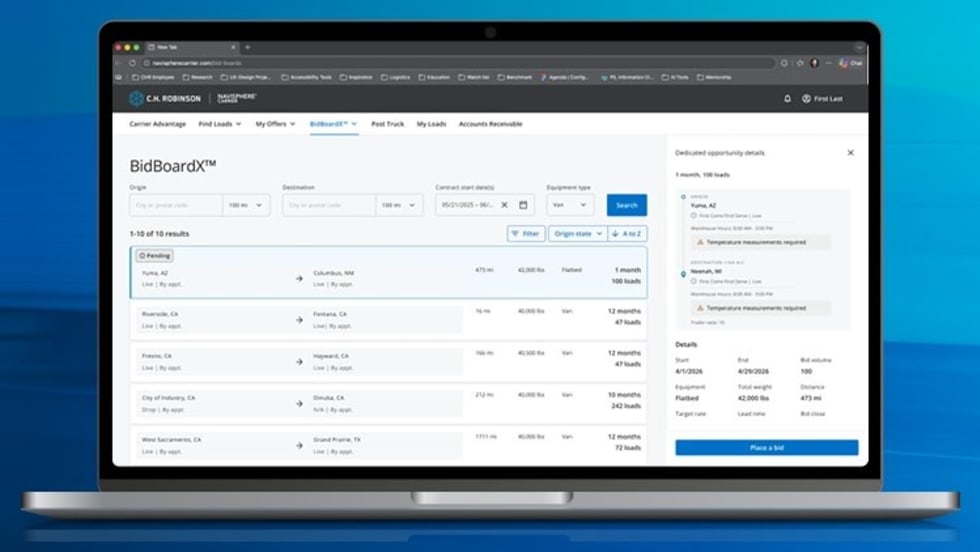

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →

Volvo Trucks Adds Unattended Over-the-Air Software Update Capabilities

The latest evolution of Volvo’s over-the-air update technology allows software updates to run while trucks are parked, helping fleets keep vehicles current without disrupting operations.

Read More →

How Waste Connections is Using Data, Telematics, and AI

How do you manage and maintain more than 18,000 connected trucks? Data. Lots of it.

Read More →