Related: COVID-19 Disruption Continues to Affect Freight, Rates

Economic Growth Steady, But Recovery's Not a 'V'

Although the economic recovery from the COVID-19 shutdown is definitely not a “V” shape, it’s growing steadily – but don’t expect to be back where we were until mid-2022, said Jeffrey Rosensweig of Emory University.

September 15, 2020

Globally, countries are expected to recover from the COVID-19 recession at different rates economically.

Photo: Screen shot of Heavy Duty Dialogue virtual event

5 min to read

Although the economic recovery from the COVID-19 shutdown is definitely not a “V” shape, it’s growing steadily – but don’t expect to be back where we were until mid-2022, said Jeffrey Rosensweig of Emory University, in a virtual Heavy Duty Dialogue session Sept. 15.

Rosensweig is director of the John Robson Program in Business, Public Policy, and Government at the Goisueta Business School of Emory University, and he kicked off HDD, put on by the Heavy Duty Manufacturers Association, with a global economic outlook.

COVID-19 Repercussions

In the U.S., some 22 million jobs were lost in March and April as the nation shut down to try to slow the spread of the COVID-19 pandemic, and we’re about halfway back, Rosensweig said. Before the pandemic, we were cruising along with about 220,000 people being laid off every week. That may sound like a lot, he said, but anything under 300,000 is considered quite good because we live in a very dynamic economy and there’s always a churn of new jobs being created while other jobs are lost.

The plummet in hospitality jobs was so deep it's not even all represented on the graph.

Photo: Screen shot of Heavy Duty Dialogue virtual event

Then the pandemic hit, businesses closed down, and we hit a new record of almost 7 million people filing first-time unemployment insurance claims during the week ending March 28.

That number has come down to a little under a million. “The good news is it’s not up around 7 million; the bad news is, it isn’t below 300,000.”

Rosensweig pointed out that the federal government’s relief package providing an additional $600 a week in unemployment benefits, on top of state benefits that average around $400 a week, has been criticized as a disincentive for some people to go back to work, including many manufacturing workers and truck drivers. However, he said, it served an important purpose in helping the economy slide even further than it did.

“Consumption is 68% of the demand in our economy. If personal consumption expenditures go down, that will collapse the economy.”

Those extra benefits have expired, and Congress has not been able to agree on an extension.

The industries hardest-hit by the COVID-19 shutdown were leisure and hospitality, as well as in health care as people put off elective procedures and wellness visits. Jobs are still off in manufacturing, as well. Although factories in general have reopened, most are not running at the same level as before the shutdown. A strong point in the jobs numbers is construction jobs.

When it comes to GDP growth, Rosensweig projects that for the U.S. economy, “even at the end of 2021 we won’t be quite back where we were before the pandemic; maybe by the middle of 2022.” He projects the GDP will grow about 3% next year as things bounce back and that growth will continue in 2022.

Financial Policy

Another factor that has Rosensweig optimistic about the economic recovery is the aggressive tactics of the Federal Reserve in stimulating the economy. The Fed, he said, has done an about-face from its previous policy of being ultra-cautious about inflation.

While it’s actually more complicated, the government has essentially been “printing money” to keep the mortgage and bond markets alive.

Jeffrey Rosensweig said the economic recover is more of a swoosh or a checkmark shape, not a "V."

Photo: Screen shot of Heavy Duty Dialogue virtual event

“For one of the few times ever, it bought not only government bonds, but also corporate bonds, which is very unusual – but it worked…. It kept a lot of corporations and our economy afloat.”

The concern is that this will lead to inflation, but Rosensweig doesn’t believe that’s a risk anytime soon. “Our economy still has a ways to go; we don’t have an excess demand for goods which would result in high prices. We still have a lot of people who are underemployed; they’re not going to demand wage increases, which also can cause inflation.”

Where this could lead to problems is further down the road, if the federal government keeps running up deficits, which could eventually lead to inflation and to higher interest rates.

“We can’t keep this expansion. But as of now, I think the Federal Reserve has done the right thing, which is to put the foot on the accelerator.”

Global and Long-Term Shifts

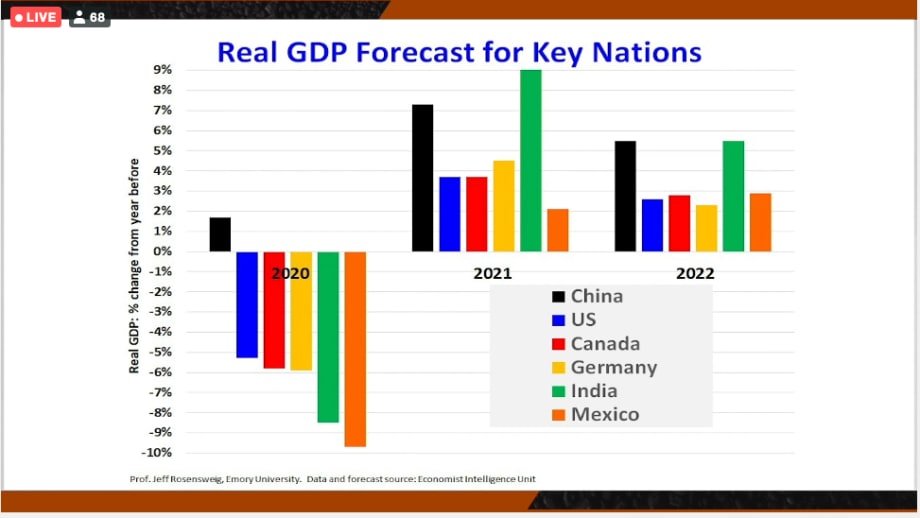

Looking at the GDP forecast for countries around the world, Rosenswieg said, you can see China, which locked down quickly and severely after the pandemic started, was able to get back to work sooner than the rest of the world and is already growing – it might even see a positive GDP for 2020 overall.

However, he said, China will not have the same type of double-digit economic growth it has seen in recent years, in part due to demographic challenges as its population ages.

India and other Southeast Asia nations may be more relevant to the global economy, with younger labor forces.

Longer term, he said the U.S. is going to face a demographic drag, as well, as there are more older workers at retirement age than there are younger people coming into the workforce.

Manufacturing, Robotics, and Offshoring

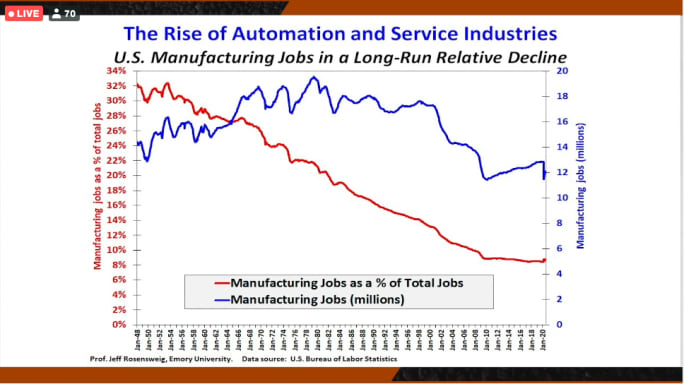

When it comes to manufacturing numbers, he said, “the great thing about manufacturing in North America is we have had this amazing technological revolution, the movement from just a lot of labor, doing things like tightening doors on cars, where now robotics does the welding.” Thanks to robotics, machine learning, and artificial intelligence, he said, “We may see another kind of industrial revolution.”

Our manufacturing sector has undergone a productivity revolution and stands poised for more gains with robotics and artificial intelligence.

Photo: Screen shot of Heavy Duty Dialogue virtual event

Manufacturing jobs in the U.S. peaked in 1979, he said. Those jobs have dropped from a 20 million peak to 12 million before COVID hit. But the vast majority of that change has been due to increases in productivity, not to offshoring, he said.

“There’s estimates that more than 80 percent of that loss in jobs is due to increased productivity, to automation, that we can produce more with fewer workers, and about 15% was lost offshore.”

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →