Related: ACT Research Says Tough Times Ahead for Class 8 Sales

ACT Research: Freight Rates Slide, 2020 Outlook Improves

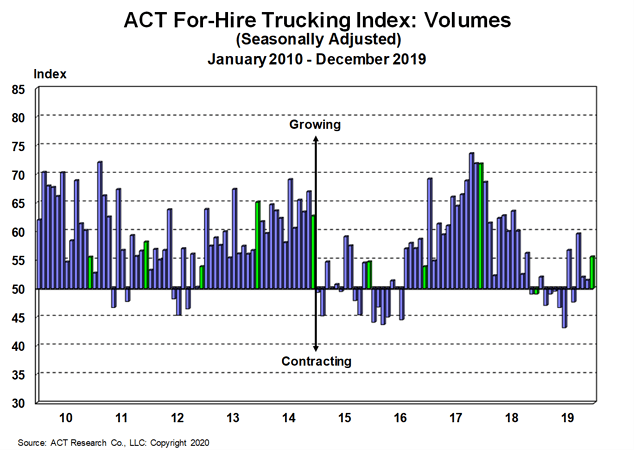

The latest reports from ACT Research show improvement in for-hire freight volumes, but also a slide in the Freight Rate Index in December and a slight improvement in the economic outlook for 2020.

January 23, 2020

Even though for-hire capacity contracted again, the Freight Rates Index slid to 48.7 in December, ACT Research said in new report.

Graph: ACT Research

3 min to read

The latest reports from ACT Research show improvement in for-hire freight volumes, but also a slide in the Freight Rate Index in December and a slight improvement in the economic outlook for 2020.

The latest release of ACT’s For-Hire Trucking Index, with December data, showed improvement in for-hire freight volumes and utilization, with 55.5 and 52.3 respective diffusion index readings, both up four points from November on a seasonally adjusted basis. But even as for-hire capacity contracted again, the Freight Rates Index slid to 48.7 in December.

“We see encouraging signs that the freight downturn is in its late stages and the market will rebalance in 2020," said Tim Denoyer, ACT VP and senior analyst. "However, the ongoing rate pressure, even as volumes ramped into the holidays, is symptomatic of ongoing excess industry capacity. Our survey respondents clearly get it, and reduced capacity for a sixth straight month, so we can pretty easily deduce that private fleet capacity additions through year-end 2019 are the main factor continuing to pressure for-hire rates.”

The ACT For-Hire Trucking Index is a monthly survey of for-hire trucking service providers. ACT Research converts responses into diffusion indexes, where the neutral or flat level is 50.

In other news, ACT Research projects that U.S. economy is poised to expand by 1.8% in 2020.

That figure is based on ACT’s State of the Industry: NA Classes 5-8 report, which provides a monthly look at the current production, sales, and general state of the on-road heavy and medium duty commercial vehicle markets in North America.

“The risk of an economy-wide recession that was a growing concern through the third quarter of 2019 has largely faded, with healthy consumer fundamentals expected to provide sufficient momentum to get through the slow patch in industrial activity,” said Kenny Vieth, president and senior analyst. He continued, “That said, the manufacturing recession continues, and the supply-demand imbalance between trucks and freight currently weighing on carrier profitability is likely to extend deep into 2020.”

Speaking about the Class 8 market, Vieth said, “For those keeping score, 2019 was the second-best year in history for Class 8 production, trailing only the EPA’07 prebuy-driven volumes of 2006. While a downturn is expected this year, the silver living is that the expected production decline in 2020 will pale compared to the 42% drop recorded in 2007.”

Regarding the medium-duty markets, he commented, “Choosing not to do a 50-year lookback, we are calling 2019 the new record year for medium-duty vehicle production, eclipsing the previous record set in 1999. And although the cycle is shallower, it isn’t so different from the heavy-duty experience over the course of last year, including lower orders, inventory building and a sharp decline in backlogs that will constrain the industry in 2020.”

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →