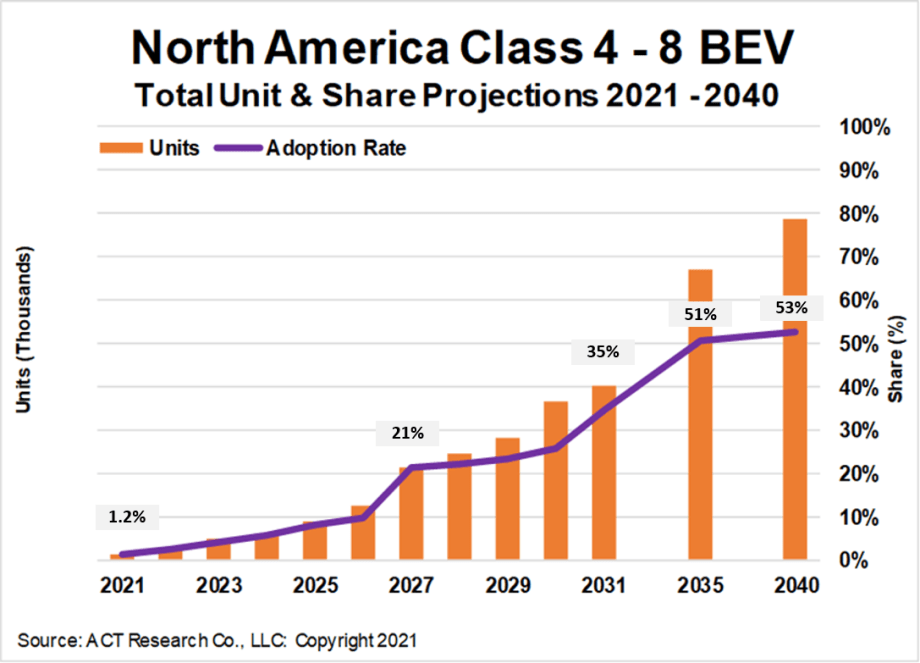

ACT: Half of Class 4-8 Sales to be BEV by 2035

Battery-electric Class 4-8 vehicles already show positive total cost of ownership compared to conventional vehicles in three-quarters of the applications examined by ACT Research in an extensive analysis.

Factors such as battery technology advancements and charging infrastructure will affect BEV adoption rates in some commercial applications.

Credit: ACT Research

Battery-electric Class 4-8 vehicles already show positive total cost of ownership compared to conventional vehicles in three-quarters of the applications examined by ACT Research in an extensive analysis. By 2030, the research firm says, that will rise to 100%. By 2040, 30% of those applications will reach price parity between BEV and conventional powertrains.

In fact, the firm projects that battery-electric vehicles will make up more than half of the Class 4-8 vehicles sold in the U.S. and Canada by 2035.

These gains will be achieved through compelling business cases, as continuing technology improvements and cost reductions make commercial battery-electric vehicles more attractive. Regulations and incentives can help, but ACT says those aren’t the dominant factor in the growth of commercial BEV market share.

These are key findings in ACT’s second edition of its Charging Forward report. ACT Research analyzed and built economic-based, total-cost-of-ownership algorithms to plot baseline, slow-case, and fast-case scenarios for adoption of 23 work applications of Class 4-8 vehicles across North America.

ACT looked at all vehicle-related costs over the full vehicle life, including purchase price, battery/fuel cell replacement, maintenance, fuel, charging infrastructure, acquisition taxes, road use taxes, insurance, and weight penalties.

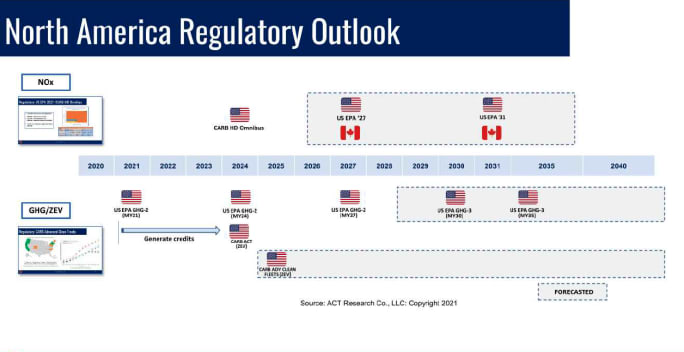

For total cost of ownership, ACT reports that a battery-electric medium-duty box truck already beats out one with a traditional diesel engine. And once new EPA diesel emissions regulations drive up traditional powertrain costs in 2027 (2024 in California), that comparison will tilt further in favor of BEVs.

“Everybody’s natural expectation is that low-GVW vehicles would see faster BEV adoption,” said Ann Rundle, who joined ACT Research a little more than a year ago as VP of electrification and autonomy, in an interview. “In fact, the higher adoption in our model is Class 6-7." ACT sees Class 4-5 shifting more to gasoline engines than BEV as diesel engine systems start to increase in cost as a result of the 2027 EPA lower NOx regulations.

In comparison, for Class 8 tractors, the TCO will favor diesel over electric until those NOx regulations kick in.

Future trends ACT identifies as key in the growth in EV adoption include:

Falling costs for batteries and fuel cells

Rising costs for diesel powertrains to meet upcoming emissions regulations

Improving powertrain efficiency for both internal combustion and EVs

Rising battery-pack energy density

Zero-emissions sales mandates

Bans on internal combustion and/or diesel engines

Refined TCO Models

This second edition took advantage of ACT’s global commercial electric vehicle analysis, “Power Up,” to refine TCO models and adoption rate forecasts for North America.

For instance, the new analysis provided better understanding of where the costs of battery packs are going and how they will be different for commercial vehicles than passenger cars, Rundle explained in an interview. There is a more in-depth discussion and reporting on regulations and incentives, which help drive adoption rates higher in the earlier years of ACT’s analysis. For instance, between when the first report was published and this second edition, more states have adopted California emissions regulations.

The new report expands on topics such as the propulsion systems and battery recycling, and there’s a new “well-to-wheel” analysis. For those who purchase the report, it comes with spreadsheets allowing users to plug in their own numbers for TCO analysis.

Upcoming emissions regulations are expected to drive up the cost of conventional diesel drivetrains, which will need additional aftertreatment.

Credit: ACT Research

Hydrogen Fuel Cells

ACT is not as bullish on hydrogen fuel cells as it is on battery-electric, saying FCEVs are challenged by durability and costs.

The report notes that for its Class 8 day-cab application model, fuel-cell electric vehicles will eventually offer better TCO than diesel, but not better than battery-electric. In the meantime, an internal-combustion-engine powertrain will have better TCO than either BEV or FCEV for this application until NOx regs tighten.

Some of the challenges the report notes on FCEV commercial vehicles include:

Existing fuel-cell systems cost an average of $350-$450 per kW, many times the Department of Energy’s goal of $80.

The system durability today is about 5,000 hours, but to be on par with diesel it would have to improve to 25,000 hours – a 500% improvement.

To put a fuel-cell system on price parity with a diesel, ACT said, would need to be 30,000 hours and a cost of $60/kW, according to Department of Energy figures.

There are challenges in building out a refueling infrastructure that would use “green” hydrogen. Current hydrogen is mostly produced through methods that are not sustainable.

What About RNG?

Rundle told HDT that although the report did not include natural gas in its comparisons, it deserves consideration.

So for its next edition, ACT will be adding a natural gas analysis — what are the CO2 emissions, what are the costs, how will tighter NOx regulations affect the balance of natural-gas engines vs. diesel or gasoline, etc. And when you factor in renewable natural gas, made from biomass or captured methane from landfills and dairy, there’s an additional greenhouse gas benefit at the source.

Rundle has been in the industry long enough to remember previous attempts at developing alternative propulsion systems, including hydraulic hybrids and diesel-electric hybrids when she was at Eaton. She’s seen EV startups such as Smith Electric come and go. When asked what’s different this time, she answered, “The technology is there. Technology has improved that much.”

Corrections: Updated Feb. 15, 2022, to make the following corrections: By 2040, about 30% of the applications will reach price parity, not "about half" as originally reported. The price for a fuel-cell system to be on parity with diesel would need to be $60/kW (a DOE figure), not $50. ACT sees Class 4-5 shifting to gasoline engines, not natural gas, as diesel engine systems start to increase.

More Fuel Smarts

EPA Proposal Could Ease 2027 Truck Costs and Buying Uncertainty

The proposal doesn't change the tougher NOx standard, but it would revise key implementation requirements that manufacturers say have driven up costs and complicated fleet purchasing decisions.

Read More →

Cummins, Paccar Ease DEF Derates After EPA Guidance

Updated diesel engine software gives truck operators more time to address emissions-system issues while staying compliant with EPA emissions standards.

Read More →

Maintenance in the Messy Middle Part 3: Biodiesel

Biodiesel can reduce emissions, improve fuel-system lubricity and use existing diesel infrastructure. But NACFE’s Messy Middle maintenance report says fleets must actively manage storage, cold-weather operation, filters and oil drain intervals to avoid problems.

Read More →

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Maintenance in the ‘Messy Middle’ Part 2: Renewable Diesel Fuel

NACFE's latest Messy Middle Powertrain Service & Maintenance report says renewable diesel gives fleets an opportunity to reduce carbon emissions without changing trucks, fueling infrastructure or maintenance practices. But technicians still need to understand several important operational differences.

Read More →

The Diesel Engine Enters NACFE’s ‘Messy Middle’

NACFE’s new Messy Middle Powertrain Service & Maintenance report says keeping modern diesel engines running now depends as much on software, diagnostics and data as traditional mechanical service.

Read More →

DTNA Software Update Gives Truckers More Time Before DEF Derates Take Effect

The changes reflect EPA guidance aimed at reducing downtime caused by emissions-system faults while maintaining compliance requirements.

Read More →

New Agentic Predictive Maintenance Report Demonstrates How Degraded Aftertreatment Systems Waste Fuel

Questar analyzed a large mixed-class fleet and discovered it was wasting as much as $30 in fuel per vehicle, per day, because of mechanically degraded aftertreatment systems.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Lessons Learned About Alternative Fuels: Start Small, Stay Flexible

Practical advice on adopting alternative fuels and ZEVs from HDT's 2026 Top Green Fleets, from renewable diesel and natural gas to electric trucks.

Read More →