2018 Fact Book: Equipment

Fleets have been buying new trucks and trailers at records rates to meet economic demand and the numbers from our 2018 Fact Book tell the story of this trucking trend.

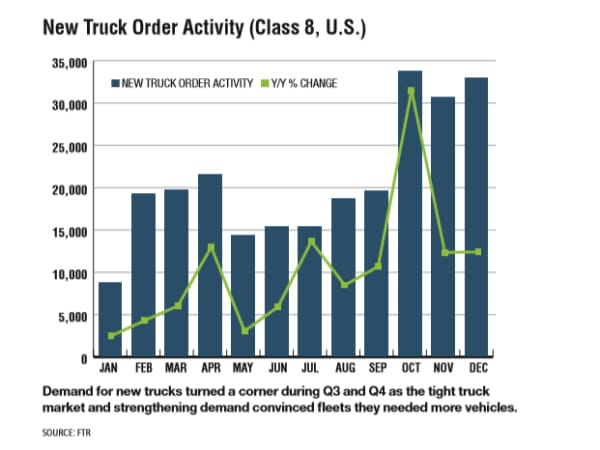

Over the course of the six-months ending in May, U.S. tractor orders posted their best-ever six-month order period in history, with orders booked at a 302,000-unit annualized rate.

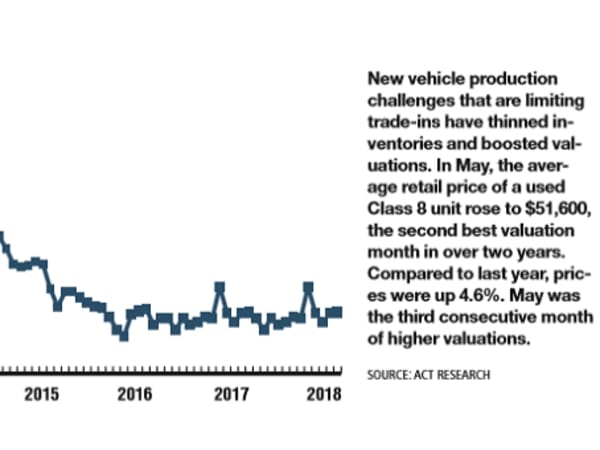

New vehicle production challenges that are limiting trade-ins have thinned inventories and boosted valuations.

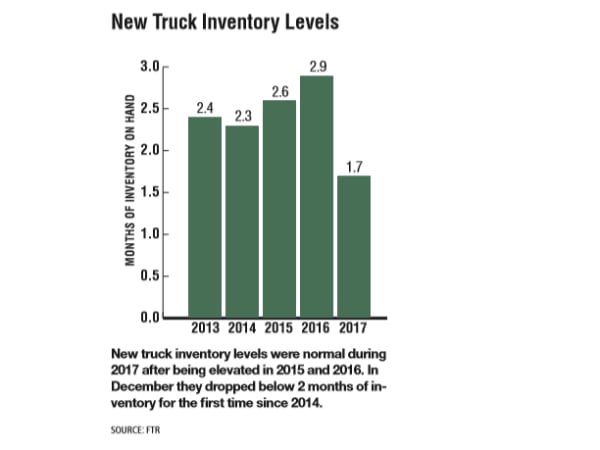

New truck inventory levels were normal during 2017 after being elevated in 2015 and 2016. In December they dropped below 2 months of inventory for the first time since 2014.

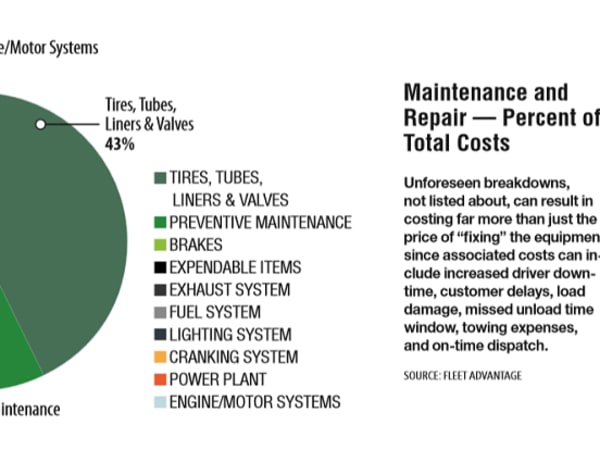

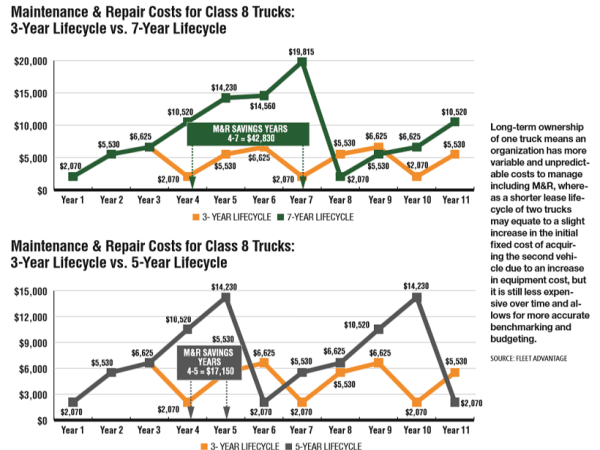

Unforeseen breakdowns can result in costing far more than just the price of “fixing” the equipment since associated costs can include increased driver downtime, customer delays, load damage, missed unload time window, towing expenses, and on-time dispatch.

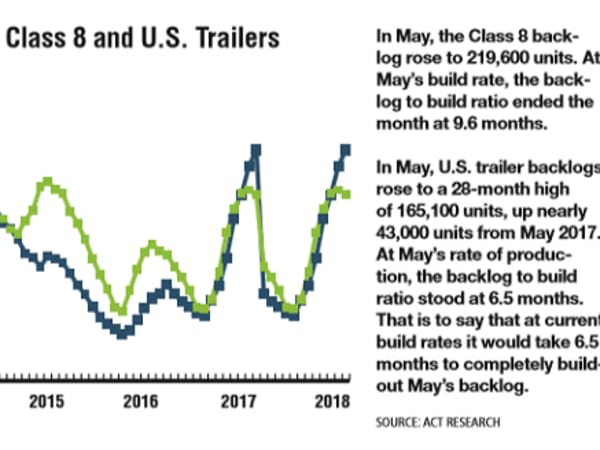

In May, the Class 8 backlog rose to 219,600 units. At May’s build rate, the backlog to build ratio ended the month at 9.6 months.

Demand for new trucks turned a corner during Q3 and Q4 as the tight truck market and strengthening demand convinced fleets they needed more vehicles.

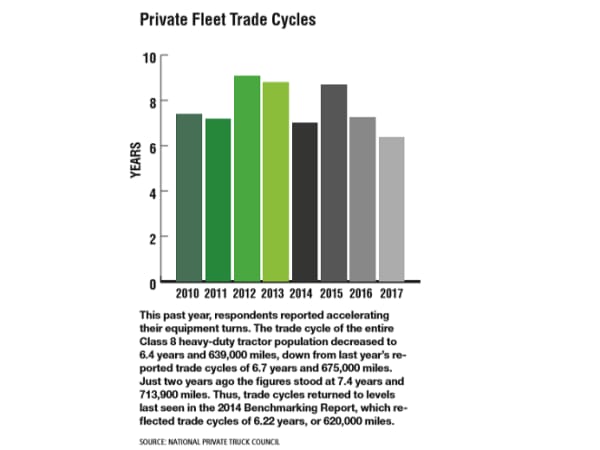

This past year, respondents reported accelerating their equipment turns. The trade cycle of the entire Class 8 heavy-duty tractor population decreased to 6.4 years and 639,000 miles, down from last year’s reported trade cycles of 6.7 years and 675,000 miles.

Long-term ownership of one truck means an organization has more variable and unpredictable costs to manage including M&R, whereas a shorter lease lifecycle of two trucks may equate to a slight increase in the initial fixed cost of acquiring the second vehicle due to an increase in equipment cost, but it is still less expensive over time and allows for more accurate benchmarking and budgeting.

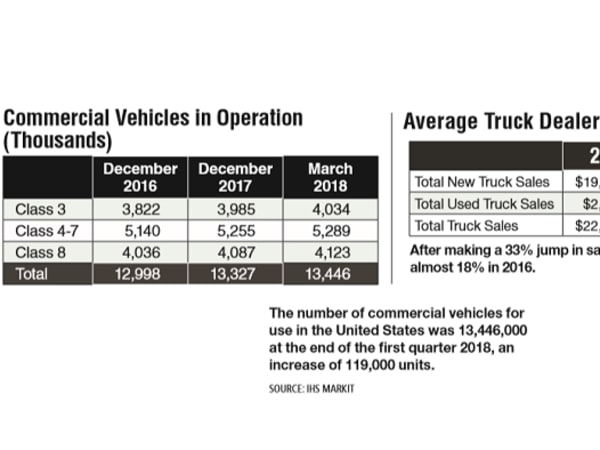

The number of commercial vehicles for use in the United States was 13,446,000 at the end of the first quarter 2018, an increase of 119,000 units.