2015 HDT Fact Book: Equipment

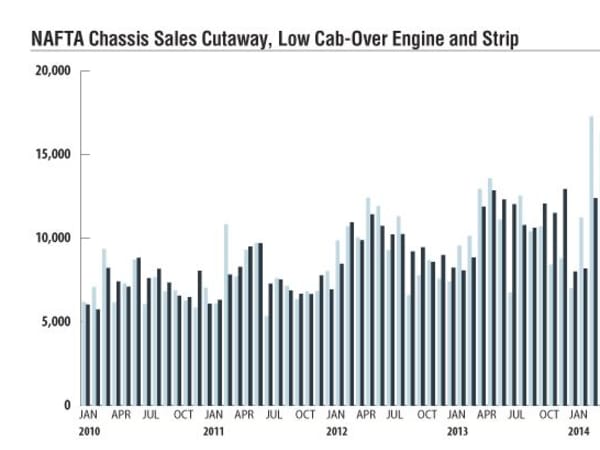

Low cab-over-engine shipments fell behind sales in 2014, but the OEMs appear to be compensating for this in 2015. Cutaway sales jumped in the first quarter of the year, but strip chassis sales are down about 20% for the year through April, according to the NTEA’s OEM Monthly Chassis Report.

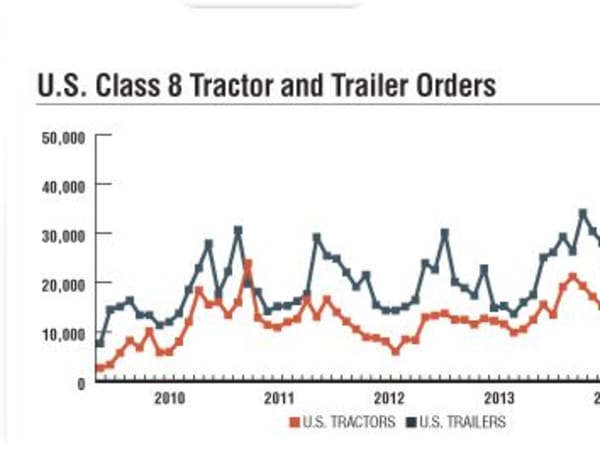

New Class 8 truck orders continued to climb in 2014, for the second-best year on record.

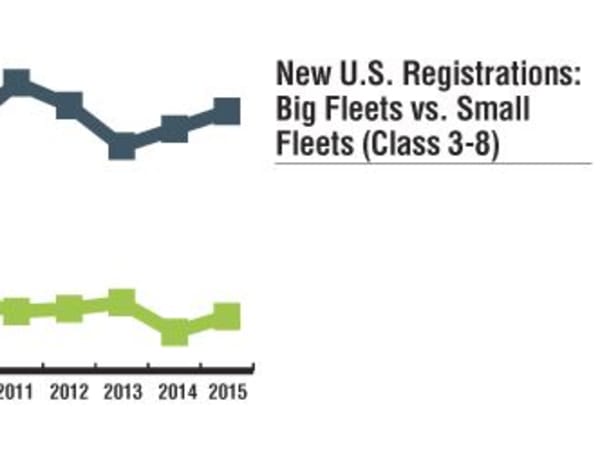

For the first five months of 2015, the small fleets made up 19.4% of the registrations and large fleets 35.9%.

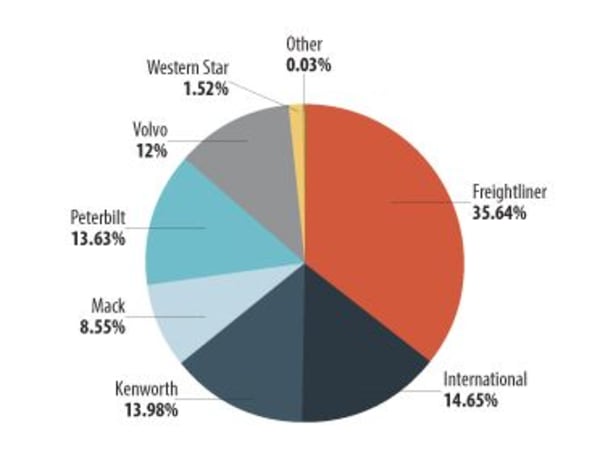

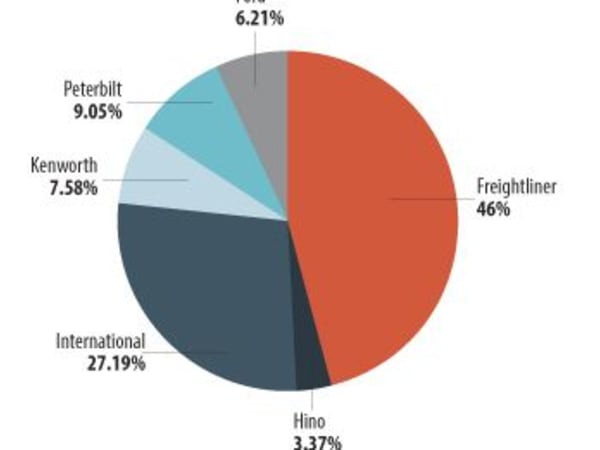

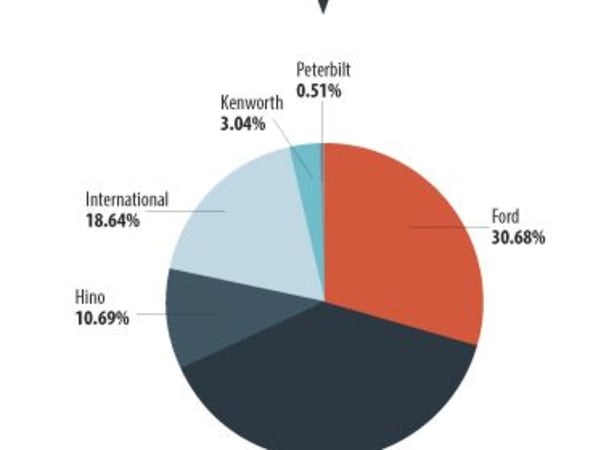

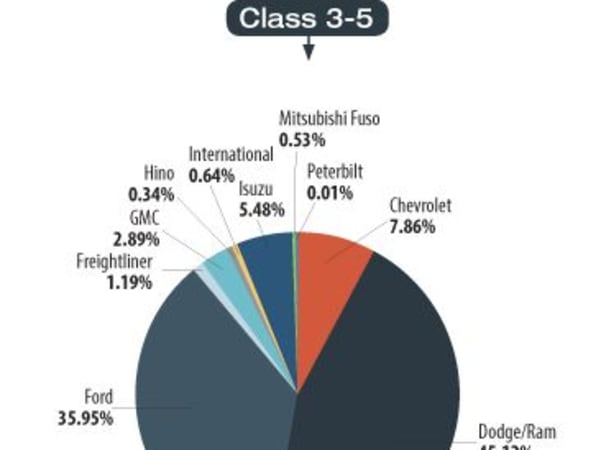

Freightliner lost a bit of market share in Class 6-8 compared to 2013. In Class 6, Ford picked up market share. In Class 3-5, Dodge/Ram extended its market share lead.

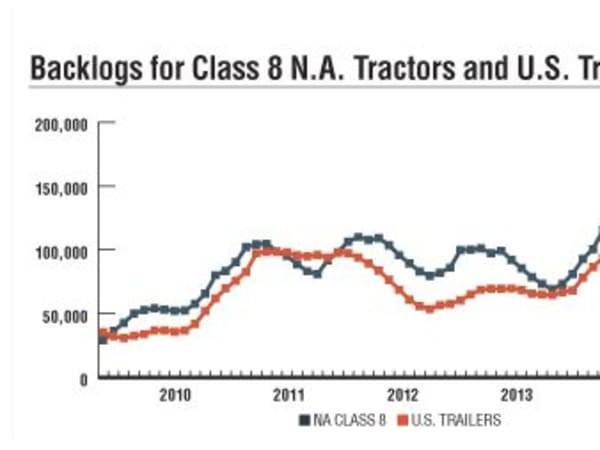

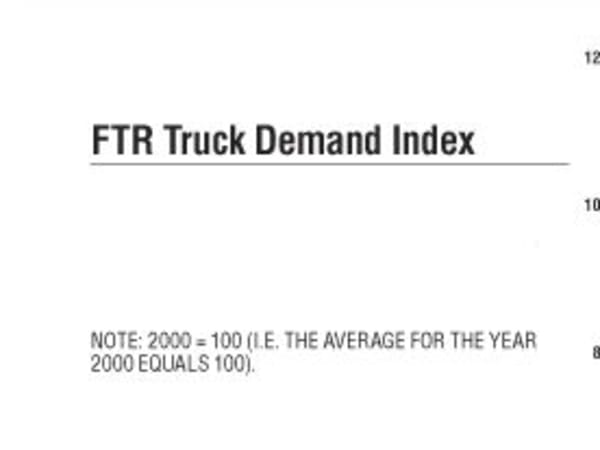

Very strong orders in the fourth quarter of 2014 have led to high backlogs, as this graph from January 2010-June 2015 reflects.

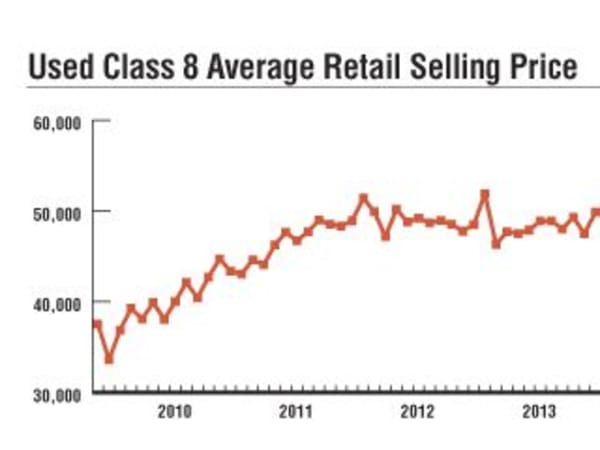

Prices for Class 8 used trucks (chart reflects January 2010-May 2015) have risen as the supply of desirable used-truck models has dropped.

Equipment orders in 2015 have fallen from the extremely high levels of last fall, but are expected to pick up again this fall, projects ACT Research.

Truck demand has remained positive for nearly the whole recovery so far. Despite this, the industry will still remain significantly below the level seen in the prior peak.

2014 retail sales showed a marked improvement over 2009, with Class 6 and 8 sales more than doubling since the recession.

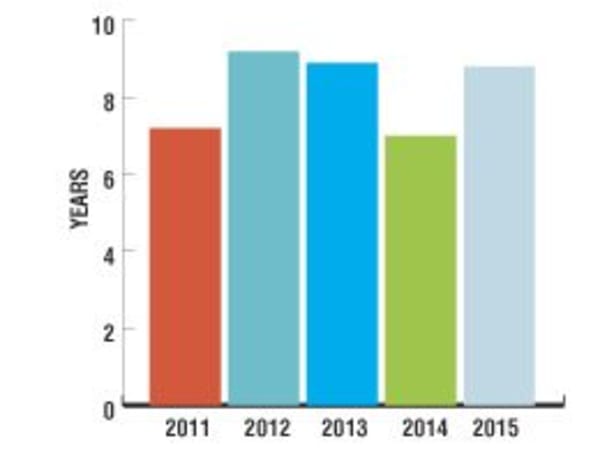

Private fleets typically keep their trucks longer than a for-hire highway carrier, as this data from the National Private Truck Council shows. (Class 8; leasing removed.)