Economic Watch: Manufacturing, Existing Home Sales, Economic Indicators Improve

UPDATED -- Three newly released reports suggest the American economy may finally be shaking off the winter doldrums that brought business activity down in the first quarter, with expectations of improvements well into the year.

UPDATED -- Three newly released reports suggest the American economy may finally be shaking off the winter doldrums that brought business activity down in the first quarter, with expectations of improvements well into the year.

Operating conditions in the U.S. manufacturing sector continued to improve during May, with strong increases in production and output complemented by further payroll growth, according to the financial information services provider Markit Economics.

Its Flash U.S. Manufacturing Purchasing Managers’ Index improved to 56.2 in May, up from April’s 55.4, the strongest reading by the survey for three months.

The latest survey data indicated continued strength in output growth, with U.S. manufacturers recording their best month-on-month increase in production since February 2011. Output has now risen consistently for over four-and a-half years and manufacturers attributed the latest production growth to a combination of higher new orders and work on outstanding contracts, according to Markit.

“The US manufacturing sector continued to gain strength heading into mid-year as supportive demand conditions led to the sharpest month-on-month increase in production for over three years,” said Paul Smith, senior economist at Markit. “This provides further confirmation that industry will aid a rebound in U.S. gross domestic product in the second quarter, and other indicators from the survey suggest that the sector has plenty of momentum heading into the summer and beyond. Total workloads are up markedly, and manufacturers are gearing up for growth by purchasing inputs at a record rate.”

New business volumes continued to rise at an elevated pace in May, amid reports of greater confidence in the marketplace, according to Markit. The domestic market appeared to be a key source of new order wins, as growth in new export sales was sustained but at a relatively modest pace.

Existing Home Sales

Existing-home sales increased for the first time this year in April, according to the National Association of Realtors.

Total existing-home sales rose 1.3% to a seasonally adjusted annual rate of 4.65 million in April from 4.59 million in March, but are 6.8% below the 4.99 million-unit level in April 2013.

“Some growth was inevitable after sub-par housing activity in the first quarter, but improved inventory is expanding choices and sales should generally trend upward from this point,” said Lawrence Yun, NAR chief economist. “Annual home sales, however, due to a sluggish first quarter, will likely be lower than last year.”

Single-family home sales inched up 0.5% to a seasonally adjusted annual rate of 4.06 million in April from 4.04 million in March, but are 7.7% below the 4.4 million pace a year ago.

Regionally, existing-home sales in the Northeast were unchanged at an annual rate of 600,000 in April, but are 6.3% below April 2013, while existing sales in the Midwest slipped 1% in April to a pace of 1.03 million and are 9.6% below a year ago.

In the South, existing-home sales increased 1% percent, to an annual level of 1.94 million in April, but are 3.5% below April 2013, while existing-home sales in the West rose 4.9% to a pace of 1.08 million in April, but are 10% percent below a year ago.

Leading Economic Indicators

The Conference Board's Leading Economic Index for the U.S. increased 0.4% in April to 101.4, following a upwardly revised 1% increase in March and a 0.5% gain in February.

“The LEI rose for the third consecutive month, driven largely by improving housing and financial market conditions,” said Ataman Ozyildirim, economist at The Conference Board. “This latest report suggests the economy will continue to expand, and may even pick up steam through the second half of the year.”

This index from the private research group is a gauge of 10 different measures of the U.S. economy.

“Despite a brutal winter which brought the economy to a halt, the overall trend in the leading economic index has remained positive,” said Ken Goldstein, economist at The Conference Board. “If consumers continue to spend, and businesses pick up the pace of investment, the industrial core of the economy will benefit and GDP growth could move closer towards the 3% range.”

Updates adds existing home sales and LEI.

More Fleet Management

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

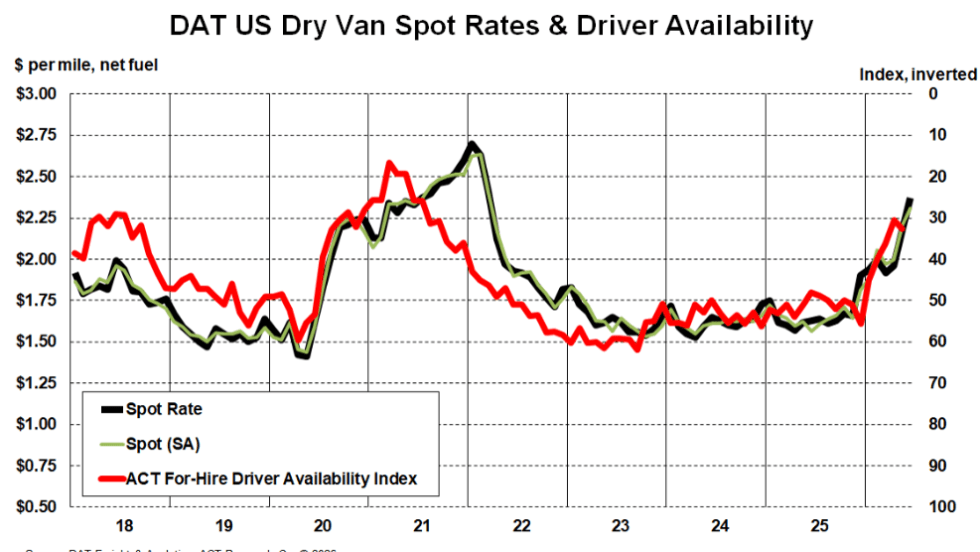

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

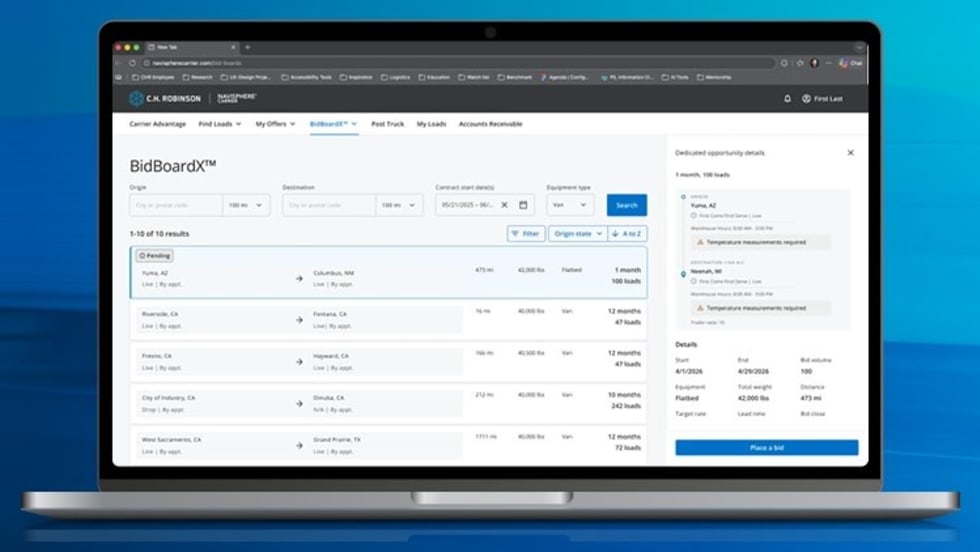

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →