Three measures of freight activity and spending were mixed, according to new figures, but the outlook for their performances has improved, according to Cass Information Systems.

Outlook for Freight Activity Seen as Improved

Three measures of freight activity and spending were mixed, according to new figures, but the outlook for their performances has improved, according to Cass Information Systems.

Evan Lockridge・Former Business Contributing Editor

Graphic: Cass Information Systems

4 min to read

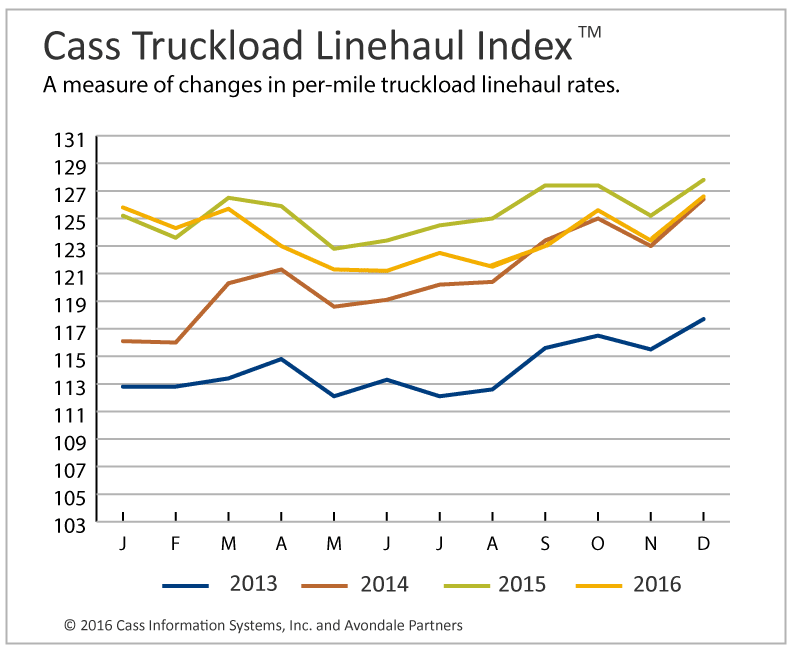

The Cass Truckload Linehaul Index, which tracks monthly changes in linehaul rates, fell 0.9% year-over-year in December to a reading of 126.6, marking ten consecutive monthly declines.

Despite this negative trend, analysts at the investment firm Avondale Partners said, "the current strength being reported in spot rates is leading us to believe that our current -3% to 1% truckload pricing forecast may need to be improved or moved to a slightly more positive outlook if the strength in spot rates continues long enough to move contract rates back into positive territory."

One possible reason is that when the December reading is compared to the month before, it improved 2.6%. That marks its biggest month-over-month gain of 2016 and its highest reading since December 2015.

Meantime, the Cass Intermodal Price Index, which tracks changes in total intermodal per-mile costs including fuel, increased 1.5% year-over-year in December to a reading of 129.2. This follows year-over-year hikes of 0.3% and 0.4% in November and October, respectively, and is 2.8% higher in December than the level the month before.

Although diesel fuel prices have recovered from their early 2016 lows, "we do not expect a significant amount of sequential strength from intermodal," said Avondale Partners. “But, the current level of demand and pricing will produce a positive year-over-year comparison for the next nine to 10 months.”

The two indices are based on data from actual freight invoices paid on behalf of freight payment process Cass Information Systems clients.

Both reports came as the December results were released for the Cass Freight Index, which measures monthly levels of shipment activity, in terms of volume and expenditures.

Its measure of shipments showed an increase of 3.5% compared to the same time a year ago but fell 1.2% from November.

The October Cass Freight Shipments Index was up 2.7%, breaking a string of 20 months in negative territory, then November fell back into negative territory, down 0.5%. However, with the December improvement, Donald Broughton, managing director, chief market strategist and senior transportation analyst at Avondale Partners, said this suggests that the October data was not a false positive but instead the beginning of a more positive trend.

"We have seen a wide range of results in the different modes, from continued volume growth in parcel and airfreight driven by e-commerce, to a sequential improvement in truck tonnage to less bad rail and barge volume overall,” he said. “Data is beginning to suggest that the consumer is finally starting to spend a little and that with the recent surge in the price of crude, the industrial economy’s rate of deceleration has eased. If the winter of the overall freight recession we’ve been in for more than a year and a half in the U.S. is not yet over, it is certainly showing promising signs of thawing.”

According to Broughton, the sequential month pattern looked a bit more ominous, but “doesn’t give us great cause for concern.” The reason is what he described as “some degree of normal seasonality at work,” and Avondale is continuing to get daily reports of stronger shipment volume in almost all modes from both hard data sources and industry anecdotes. "It also looks far less troubling when compared to the seasonality in 2013, 2014 and 2015,” he said.

And while the Cass Freight Expenditures Index remained in negative territory, falling 3% in December compared to a year earlier and down 1.1% versus the month before, it also gives Broughton some hope.

“Expenditures, or the total amount spent on freight, were still down, but as was true in October and November, this was less than the rates of contraction in May, June, July and August; down 10.1%, 8.8%, 5.1% and 6.3%, respectively,” he said. “We see this... as a result of the steady increase in the price of fuel over the last six months and the recent rise in the price of crude should only add to this positive bias, but we are also seeing some improvements in the pricing power of truckers and intermodal shippers."

He pointed to numbers from the Cass Truckload Linehaul Index (which does not include fuel) that showed only a 0.9% year-over-year decline in November, far less than the 3.5% drop it posted in September. Also, the Cass Intermodal Price Index (which includes fuel costs) faired even better, marking the third year-over-year increase after 21 consecutive months of decline.

Helping to drive December shipment volume was parcel volume associated with e-commerce continuing “to show outstanding rates of growth, with both FedEx and UPS reporting strong U.S. domestic volumes,” according to Broughton.

He said rail volumes have been part of the weakness, but have become increasingly less bad, and in recent weeks have turned slightly positive. As for trucking overall, volumes are mixed, as tonnage continues to be slightly positive and load volume continues to be slightly negative.

More Fleet Management

'Beyond Compliance,' Regulations, Driver Coaching on ATRI’s 2026 Research List

The American Transportation Research Institute will examine driver coaching, regulatory impacts — including the "Beyond Compliance" concept —and weather disruptions that shape trucking operations.

Read More →

Fleet Advantage's Brian Antonellis on the Growing Need to Replace Old Trucks

Fleet Advantage's Brian Antonellis says it's time for fleets to get back to the fundamentals of good maintenance practices. And that includes replacing older, inefficient equipment.

Read More →

Truckstop.com Adding to Open Deck, Heavy Haul Offerings

Load matching for flatbed, lowbed, oversize and overweight loads can't be automated like basic van freight, but Truckstop.com is adding more high-tech tools to help.

Read More →

Trucker Path, Truckstop.com Expand Load Access Partnership

An expanded Trucker Path and Truckstop.com integration brings more freight opportunities into the TruckLoads app while emphasizing security and network quality.

Read More →

Truckload Rates Hit Two-Year Highs as Diesel Costs Surge, DAT Says

Strong March freight demand combined with a spike in fuel costs pushed both spot and contract truckload rates to their highest levels in more than two years.

Read More →

The AI Conversation You Need to Have with Your TMS Provider

Everyone’s talking about AI — but is your transportation management system actually built for it?

Read More →

Kriska Buys Fellow Canadian Carrier Sharp Transportation Systems

Being part of KTG will allow Sharp to expand and improve its services.

Read More →

Bill in House Would Raise Minimum Insurance for Motor Carriers to $5 Million

The Fair Compensation for Truck Crash Victims Act would increase insurance requirements for interstate motor carriers by nearly seven times.

Read More →

FTR Trucking Conditions Index Hits Four-Year High in February

Strong freight rates push TCI to 10.2, but FTR expects fuel-price volatility to skew March results.

Read More →

C.H. Robinson Offers Carriers Relief as Diesel Prices Surge

C.H. Robinson is waiving fees on fuel cards and cash advances for April and May, aiming to help carriers offset rising diesel costs tied to geopolitical instability.

Read More →