Latest Freight Shipment, Spending Levels Show Economic Uncertainty

Freight shipments across all U.S. domestic modes continued improving in August but remain weak, according to the latest Cass Freight Index, while freight spending moved lower again with both resulting in mixed feelings when it comes to their economic impact.

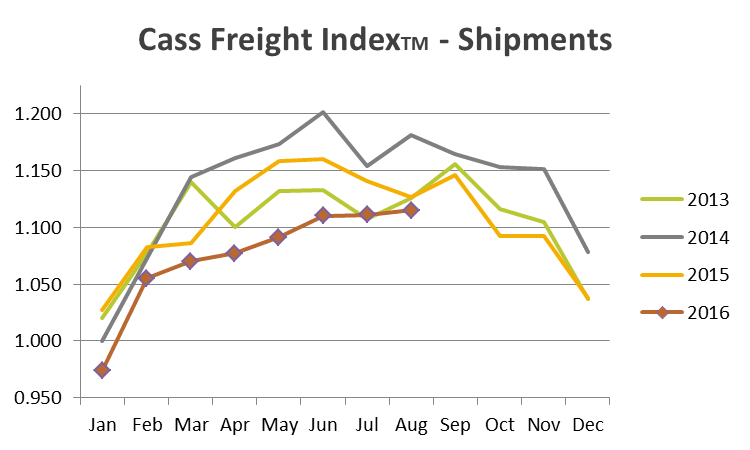

Graphic: Cass Information Systems

Freight shipments across all U.S. domestic modes continued improving in August but remain weak, according to the latest Cass Freight Index, while freight spending moved lower again with both resulting in mixed feelings when it comes to their economic impact.

Its measure of shipments increased 0.4% compared to July for a reading of 1.115, the highest level since last September, but is down 1.1% from August 2015, the 18th straight year-over-year decline.

According to the report, this most recent activity is mostly related to e-commerce, with lower levels of expansion being experienced in transit modes serving the auto and housing/construction industries. Also the increase in the month-over-month performance offers “a glimmer of hope that the contraction in volumes may be getting closer to an end.”

Figures also show freight spending declined during August, 3.3% from the month before and fell an even larger 6.3% from August 2015 for an index reading of 2.278, its lowest level since January.

“We continue to see this weakness as driven by the excess of capacity in most modes: trucking, rail, air freight, barge, ocean container and bulk,” said Donald Broughton managing director, chief market strategist and senior transportation analyst at the investment firm Avondale Partners, who provides analysis in the report. “The weakness is also driven in part by the ongoing decline in diesel and jet fuel and corresponding fuel surcharges that influence pricing realized by shippers.”

He says the August increase in freight volume certainly wasn’t driven by railroads, as carloads and intermodal shipments both declined, while tonnage moved by trucking appears to be growing, though it’s still down on a year-over-year basis.

Broughton says when it comes to freight rates in August, at first blush it appears that in most modes the gap between spot pricing and contract pricing appears to be closing slightly, but rather this is more a function of slight declines in contract pricing than it is a function of improvements in spot pricing.

“We see little reason to predict a change in course or material strength in either the contract or spot rates for most modes,” he said. “Exceptions to this do remain in the parcel marketplace and forms of expedited transit supporting e-commerce.”

All this activity, Broughton says, comes amid a backdrop where the U.S. economy continues to be in a state of transition. In the report, he says:

“After the explosion in fracking activity (pun intended) drove the first industrial-led recovery (2009-2014) in the U.S. since 1961, we have been patiently waiting for the consumer to take the baton of leadership in economic growth. Fracking in the U.S. has been so successful that it drove the worldwide price of crude down and positioned the U.S. globally as the world’s single largest oil producer. It also drove the North America price of natural gas to record lows not seen since the 1999 El Nino-induced levels. With the dramatic drop in crude and natural gas prices, the financial incentive to drill and frack additional wells also dropped, and the U.S. slipped into an industrial recession in March 2015. Nearly all of us practicing the dismal science of economics began predicting in the Spring of 2015 that as the price of oil and natural gas fell, the consumer would take the increase in disposable income—created by the decreases in the costs of their daily commute and heating and cooling their house—and spend it. Why? Because since the end of World War II, the greatest predictor of consumer spending, expansion or growth, was the expansion or growth of consumer disposable income. But instead of following the playbook, most U.S. consumers have been choosing to pay down debt and increase their savings rate. Simply put, the consumer has not yet picked up where the industrial economy left off.”

Adding to the recent malaise in trucking and the economy, Broughton says, is that business inventories have been high, subtracting from gross domestic product growth for five consecutive quarters.

“This is the longest stretch outside of a recession since 1956-57 and the largest in magnitude since 1995. We expect de-stocking to continue into the third quarter in retail….[but] we remain concerned about elevated levels of cars on dealer lots, and we acknowledge continued efforts to streamline finished inventory in most machinery sectors,” he says.

Broughton notes overall inventory levels remain elevated compared to sales, “but with further improvement on many ratios in the second half of the year, which we expect, and unless demand takes another step down, we believe the persistent drag of de-stocking should progressively lessen as we enter 2017.”

Despite this more slightly upbeat note, for at least the second half of the year, Broughton is concerned about consumer spending, which drives a huge chunk of the economy and is responsible for moving a large amount of truck freight.

“The U.S. consumer has been saving and paying down debt with this disposable income for over six quarters. By this holiday season, we expect them to begin to spend at least part of their income. If not, the risk of an overall recession grows,” he says.

According to him, the longer the consumer saves and pays down debt, the more likely it is that the U.S. falls into a recession. But, the longer the consumer saves and pays down debt, the shorter and more mild the recession will be since there will be less excess to clean up.

More Fleet Management

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →

Volvo Trucks Adds Unattended Over-the-Air Software Update Capabilities

The latest evolution of Volvo’s over-the-air update technology allows software updates to run while trucks are parked, helping fleets keep vehicles current without disrupting operations.

Read More →

How Waste Connections is Using Data, Telematics, and AI

How do you manage and maintain more than 18,000 connected trucks? Data. Lots of it.

Read More →

Why Fleet Data Matters More Than Ever at Waste Connections [Watch]

Waste Connections' Chuck Palmer explains how telematics, predictive maintenance, safety analytics, and AI help keep vehicles on the road and drivers safe in this episode of HDT Talks Trucking.

Read More →

NMFTA Launches Free, Anonymous Cybersecurity Threat Report Portal

Organizations are encouraged to anonymously report freight fraud, cargo crime, and cyber threats while gaining visibility into incidents reported across the transportation sector.

Read More →