Economic Watch: 3 Reports Show Uneven Freight Movements

Taken separately, new reports on freight movements in the U.S. on freight volume, shipper spending and even the spot market seem to run almost counter to one another. A deeper dive into the analysis shows why activity has slowed but is not widespread.

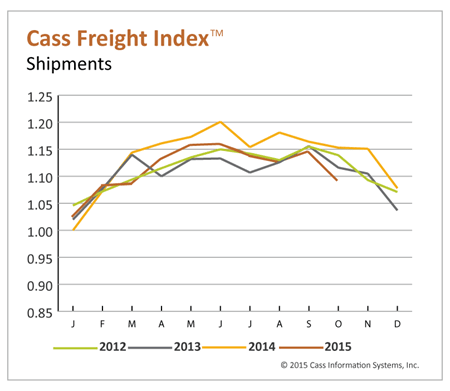

Cass Freight Index of shipments. Credit: Cass

Taken separately, new reports on freight movements in the U.S. on freight volume, shipper spending and even the spot market seem to run almost counter to one another. A deeper dive into the analysis shows why activity has slowed but is not widespread.

Total spending on shipments and the number of shipments for North American freight fell in October, according to the Cass Freight Index. Its measure of shipments fell 5.3% from a year earlier and posted 4.7% drop from September. This put the index at a level of 1.092, the worst October performance since 2011, and the lowest reading since March.

Also, the Cass measure of freight expenditures fell 8.7% last month from the same time in 2014, while showing a 2.2% drop in October of this year from September. That puts this measure at 2.435, also the lowest October reading since 2011.

The October decline in shipments is much sharper than in recent years and can be directly correlated to falling imports and exports as well as decreased domestic manufacturing levels, according to Rosalyn Wilson, supply chain expert, and senior business analyst with the management services firm Parsons, who provides analysis for the report.

“Burdened by bloated inventories, and under the shadow of a possible interest rate increase by the Federal Reserve, businesses cut back on new orders placed in the last three or four months. This is resulting in lower import volumes, less freight to move and faltering industrial production,” she said.

The drop in freight payments was the third in the last four months.

“While some of this month’s decrease comes with the drop in shipments, spot rates have also impacted October’s results,” Wilson said. “At this point in time there is abundant capacity in the trucking sector, which has depressed spot rates. Trucking companies are reporting that new contracts are yielding only 2% to 3% rate increases going into 2016. Dedicated carriage contracts are faring slightly better for the carriers, with an average of a 3% to 4% percent rise in rates. Carriers are still reporting that they are unwilling to lose a good customer over a few percentage points.”

The drop in spot market freight rates Wilson was referring to can be clearly seen in new figures released by the freight matching service provider DAT Solutions.

The DAT North America Freight Index also showed spot market freight volume declined 9.7% in October.

Line haul rates fell 5.7% for vans, 5.6% for reefers and 5.4% for flatbeds, compared to October 2014. Total rates paid to the carrier declined by 15% year-over-year, partly due to a 48% decline in the fuel surcharge, which comprises a portion of the rate.

When October is compared to the month before, line haul rates on the spot market followed volume trends by equipment type, falling 2.6% for vans, 4.5% for reefers and 1.7% for flatbeds.

The latest figures are a common seasonal pattern, according to DAT. However, the company notes while freight volume fell below same-month levels of the past five years, total volume for the year to-date has exceeded the same period for every year prior to an atypical 2014.

By equipment type, compared to the previous month, van freight availability declined 13%, refrigerated trailers lost 16%, and flatbed volume slipped 4.5% lower.

Compared to the record spot market volume of 2014, freight was down 44% in October. By equipment type, year over year, van demand was down 42%, reefer volume fell 34%, and flatbeds dropped 50%, compared to October 2014.

Finally, a third report that looks a little further back into the overall freight hauling picture in the U.S. shows the recent slowdown in activity isn’t limited to last month.

The federal government’s Freight Transportation Services Index (TSI), which is based on the amount of freight carried by the for-hire transportation industry, rose 0.2% in September from the revised and now unchanged August level.

Despite the small to zero increases in the index’s most recent two months, the level of freight shipments in September measured by the Freight TSI, 123.4, was 0.1% below the all-time high level of 123.5 in November 2014. And September was 1.5% higher than September 2014.

At first blush, this almost runs counter to what Wilson detailed in her report, but there is more to the overall picture.

As manufacturing levels have declined, along with shipments from this sector of the economy, another area has been increasing – retail spending, a bigger driver of the American economy and truck freight.

According to Wilson, consumer sector goods are, by far, the strongest in the market now.

“In many ways this is the silver lining in the storm clouds, because it means that consumers are still in the game,” she said. “Consumer spending, which accounts for more than two‐thirds of U.S. economic activity, grew 3.2% in the third quarter after expanding at a 3.6% pace in the second quarter.”

More Fleet Management

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

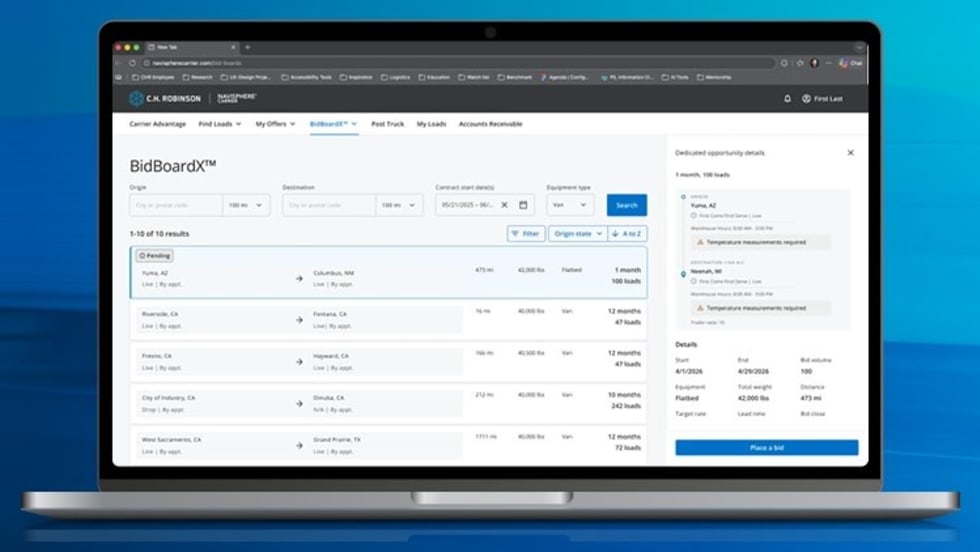

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →

Volvo Trucks Adds Unattended Over-the-Air Software Update Capabilities

The latest evolution of Volvo’s over-the-air update technology allows software updates to run while trucks are parked, helping fleets keep vehicles current without disrupting operations.

Read More →

How Waste Connections is Using Data, Telematics, and AI

How do you manage and maintain more than 18,000 connected trucks? Data. Lots of it.

Read More →