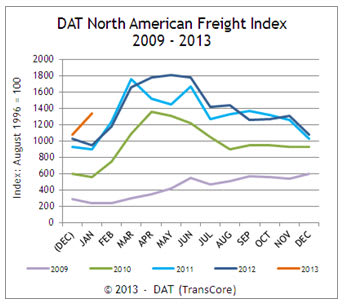

Spot Freight Index Shows Unusual Strength in January

Reaching the highest-ever volume for the month of January, the DAT North American Freight Index increased 42% last month compared to January 2012. Freight volume was unusually robust for the season, exceeding December levels by 24%

This is the first time DAT's Spot Freight Index has shown an increase in freight availability from December to January.

Reaching the highest-ever volume for the month of January, the DAT North American Freight Index increased 42% last month compared to January 2012.

Freight volume was unusually robust for the season, exceeding December levels by 24%. This is the first time the Freight Index has shown an increase in freight availability from December to January. Over the past 10 years, there has been a 13% average decline in freight levels between those two months.

The DAT North American Freight Index is a measure of spot market freight availability in the U.S. and Canada.

Seemingly Contradictory Market Activity

Several things contributed to the seemingly contradictory market activity reflected in the DAT North American Freight Index in January — that is, a big increase in the volume of freight without a corresponding rise in rates.

"According to Mark Montague, DAT's industry pricing analyst and chief market-watcher, extraordinary things are happening with higher levels of exports to Brazil, China, and Mexico," explains David Schrader, senior vice-president of DAT's freight-matching business in Portland, Ore. "Much of this export freight is industrial freight, which tends to be spot-market freight.

"Also, according to industry reports, the 'contract marketplace' — i.e., freight shippers directly contracting loads out to carriers — shrank by 2.5% in January. This would have forced capacity into the spot market, which, while robust, is smaller than the contract marketplace. The net-net of all this is that loads as well as trucks (capacity) greatly increased on the spot market in January."

The net impact on spot market rates through most of January was negative, as the excess capacity in the marketplace competed for available loads. When it comes to contract rates, shippers appeared to be cautious about committing to higher contract rate volumes due to conflicting signals about consumer demand, Shrader says. "Additionally, when fuel prices increased recently, carriers realized the need to adjust pricing. That is contributing to higher fuel surcharge numbers (calculated) in most regions of the U.S, with the result that the overall net rate rising."

Mismatched Demand and Capacity

It's no unheard of for the spot market to grow even while freight volume is contracting, Schrader says. "The spot market often absorbs the effect of a mismatch between demand and available capacity in the larger freight market," he explains. "This mismatch can occur because of unexpected or large-scale changes in the freight marketplace or even in the economy. Specific markets, regions, and/or equipment types may be affected disproportionately, or there may be a broad trend among shippers to respond to economic conditions in a certain way." On a month-over-month basis, the unusual trend in freight availability affected the three major trailer types to differing degrees: van loads increased 16%, refrigerated freight volume increased 14%, and flatbed freight availability rose 28%. Compared to January a year earlier, freight volume increased 36% for vans, 32% for reefers and 7.9% for flatbeds.

Despite strong freight volumes, truckload capacity remained relatively loose in the spot market, so rates followed a somewhat typical seasonal pattern of a January decline that was most significant for vans and flatbeds. Van rates dropped 2.4% and flatbed rates slipped 2%, not including fuel surcharges. Reefer rates remained stable in January compared to December. On a year-over-year basis, van rates declined 2.4% and flatbeds lost 5.7%, while reefer rates rose 8.6%.

Meanwhile, Schrader says, February data is shaping up as you might expect in a dynamic market. DAT is seeing increased demand regarding spot freight plus tightened capacity, contributing to a rise in the line-haul rate.

Looking ahead to March, DAT believes the best combination of load volume and a favorable ratio of outbound loads should be found in Ohio, Illinois and Indiana in the Midwest, as well as in the Southeastern states of Georgia, North Carolina and Alabama.

More Drivers

Prime Inc. to Open $7.9M Flagship Used-Truck Dealership

A new driver-focused facility to sell Prime Inc's used trucks and trailers will be the first purpose-built location in the company's history.

Read More →

Short Takes: Inside K&B’s Truck Safety Tech

Listen to learn how K&B Transportation uses cellphone-blocking technology, speed management systems, weather geofencing, bridge avoidance tools, and more to improve driver safety.

Read More →

Nussbaum Expands Driver Compensation with Pay Raises, Profit Sharing

Nussbaum Transportation said its latest compensation package could push first-year driver earnings above $90,000 in key hiring markets.

Read More →

Listen: Inside Modern Fleet Safety: AI, Cameras & Speed Control at K&B Transportation

Fleet safety is evolving fast—and technology is at the center of it. Learn how a former commercial vehicle enforcement officer turned director of safety at K&B Transportation is embracing real-world safety technology.

Read More →

Maverick Announces 2026 Driver Pay Raises

New raises for Maverick Transportation drivers will take effect on May 31, 2026.

Read More →

Illinois Trucker Indicted for Nearly $22,000 in Ohio Turnpike Toll Evasion

Authorities say an Illinois trucker avoided paying tolls for two years, and now faces felony charges, possible prison time, and forfeiture of his Freightliner tractor.

Read More →

New Trojan Driver Cargo Theft Scam Bypasses Carrier Vetting Systems

Cargo theft rings plant operatives as drivers inside legitimate, fully vetted carriers, then execute coordinated thefts that look like a traditional straight theft from the outside.

Read More →

WIM, Trucker Path Name Top 3 Women-Friendly Truck Stops

ATA’s Women In Motion Council and Trucker Path highlight three truck stops that meet all seven safety-focused criteria and rank highest among female drivers.

Read More →

FMCSA Extends Paper Medical Card Exemption … Again

Five states still aren't ready to accept commercial driver medical exam information directly from the medical examiner's registry.

Read More →

Mack Launches Digital Driver Guide for Chassis-Specific Truck Info

Mack’s new, virtual owner’s manual delivers VIN-based, on-demand guidance for vehicle systems via web, app, and soon in-cab displays.

Read More →