Analysis: Lessons From Interesting Times in the Spot Market

Traditionally, transportation and logistics managers start planning in earnest for the coming bid season with a look back at the previous year for indicators about the future. Well, consider that tradition officially “bucked.”

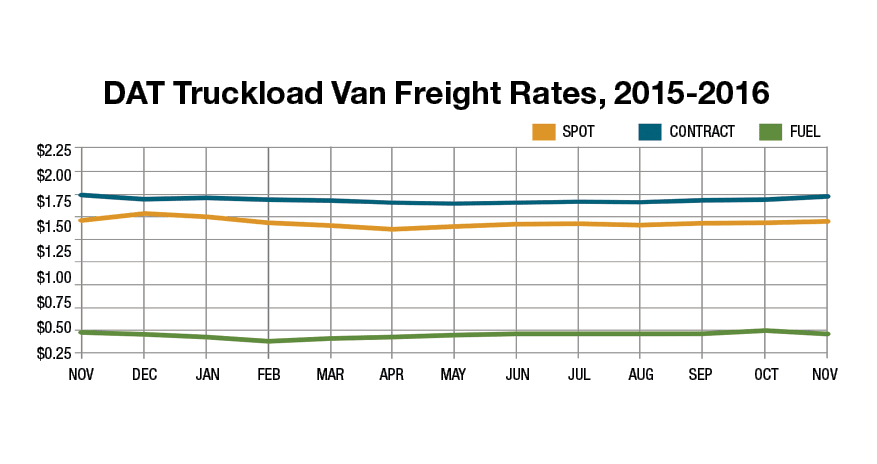

Source: DAT Solutions 2016

Traditionally, transportation and logistics managers start planning in earnest for the coming “bid season” with a look back at the previous year for indicators about where demand and capacity might be heading in the future.

Well, consider that tradition officially “bucked.”

First, bid season is getting harder to define. Requests for proposals (RFPs) can – and do – come down at any time. Second, transportation managers are scratching their heads over whether there’s anything they can learn from the last 12 months, a truly unusual year for spot truckload freight volume and rates.

During the first half of 2016, the amount of available freight seemed to be in a state of constant transition, with an economy stalled between growing and shrinking. Then something unusual happened.

In July, when freight volume typically begins a gradual decline, activity never really tapered off. In fact, the number of available van and refrigerated loads on the spot market surged. Van freight volume increased 17% while reefers gained 5.2% compared to July 2015, according to DAT Solutions, which operates the DAT network of load boards. It continued moving higher each month with year-over-year of 51% and 44%, respectively, in October.

Why? In hindsight, there were several factors.

First, freight volume on the spot market was so low to start the year that big 3PLs and freight brokers were able to easily undercut the rates of contract carriers. As contract carriers lost market share to 3PLs, that freight shifted onto load boards.

Second, a number of disruptive events in the second half of the year caused spikes of demand in certain markets. The bankruptcy of Hanjin Shipping in August sent ripples from the West Coast through the supply chain and increased amounts of inventory transfers throughout the fall. Bad weather, particularly flooding in Louisiana and the Carolinas, generated demand for emergency relief followed by construction supplies and equipment. Bumper crop yields from non-California states increased the amount of fruits and vegetables to be moved. Those loads all went onto the spot market.

Third, the surge of online holiday shopping has led to e-commerce and parcel delivery companies consolidating loads and using the spot market to move them from hub to hub. The week after Thanksgiving had the highest spot truckload freight volumes seen in the past two years.

Finally, the economy generally improved in the second half of 2016, with higher employment numbers, rising wages and more consistent manufacturing output. We’re no longer seeing volumes rise because loads are moving from the contract side to a load board, but because there’s more freight to move as a whole.

One takeaway for carriers is that higher van and reefer freight volumes on the spot truckload market did not necessarily translate to higher rates. For example, in August, when van and reefer volumes were up in excess of 30%, the van rate edged down 0.7% to $1.41 per mile while the reefer rate lost 1.7% as a national average.

So what can carriers learn?

1. Watch the gap between shipper-to-carrier contract rates and the spot rates. A wider gap is an opportunity for freight brokers, who can offer competitive pricing to shipper customers without paying more to carriers.

2. Small carriers have been able to get by with a lower rate in the short term because fuel has been relatively cheap. If the cost of fuel increases (the Energy Department is forecasting a 16.6% rise in 2017 over 2016), the rising surcharge would narrow the gap between the spot and contract rates, making it easier for contract carriers to adjust their pricing and avoid losing share to freight brokers and 3PLs.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →